June 5, 2026

Choosing the best AML software for startups means weighing deployment time, AI quality, pricing transparency, and whether the tool was built for your scale - not just for tier-one banks.

Here's the quick view.

Anti-money laundering (AML) software is a category of compliance technology that helps financial institutions, fintechs, and payment companies detect, prevent, and report suspected money laundering activity - and meet the regulatory obligations that come with it.

At its core, the best AML software solutions for a new startup combine transaction monitoring, sanctions and PEP screening, customer risk scoring, case management, and regulatory reporting into one connected workflow.

Modern platforms go further by layering in machine learning and AI to reduce false positives, prioritize high-risk alerts, and adapt to emerging financial crime patterns faster than rule-based systems ever could.

The AML compliance market has grown significantly. Regulators across the US (FinCEN/BSA), EU (AMLA, 6AMLD, PSD2), UK (FCA), and emerging markets are tightening scrutiny across the spectrum. For payment companies and fintech startups specifically, AML software must handle high transaction volumes in real time, integrate quickly with existing infrastructure via API, and support ongoing compliance across multiple jurisdictions; all without requiring a 10-person compliance team to operate it on day one.

Most payment startups don't fail because of a bad product. They fail because compliance catches them off guard.

Here's what happens without a proper AML setup: You onboard customers, process transactions, and grow. Then a regulator audit flags gaps in your monitoring. A card scheme hits you with fines for suspicious transaction volumes. Or a money mule network quietly processes stolen funds through your platform for weeks before you notice; after chargebacks have already arrived.

The consequences aren't theoretical. AML fines globally reached billions of dollars in 2024-2025, and the EU's AMLA framework became operational in mid-2025, extending AML obligations more aggressively across digital finance. Non-compliance doesn't just cost money. It can mean license revocation.

Beyond regulatory risk, the operational burden of manual AML processes grows faster than the team does. Reviewing transaction alerts by spreadsheet, running batch screenings overnight, and filing SARs by hand works at 500 transactions a day. It doesn't work at 50,000. Startups hit a wall, and when they do, they're already behind.

The right AML software solves this at the root, monitoring transactions in real-time, surfacing true risk while keeping a clean audit trail and scaling with your transaction volume; all without proportionally increasing headcount.

Next-generation platforms now process over 2 billion transactions across 188 countries, demonstrating that AI-native AML compliance has moved well beyond the pilot stage into production-proven, global-scale deployment accessible to payment startups from day one.

The best AML software solutions for a new startup aren't one-size-fits-all. Different companies have different exposure, different regulatory environments, and different technical constraints. But if your startup touches payments in any way, the question usually isn't whether you need AML software - it's which kind, and when.

Here's who needs what:

An early-stage fintech applying for an EMI (Electronic Money Institution) license or payment service provider authorization will face direct requirements for transaction monitoring capabilities from day one.

Regulators and card schemes expect to see a documented, working AML system, not a promise to build one.

Startups in this position need a tool that deploys fast (days, not months), fits within an early-stage budget, and produces compliance outputs that satisfy a regulatory review.

Payment facilitators (PayFacs) and merchant acquirers hold direct liability for the merchants they onboard and process for. Approximately 3% of new digitally-boarded SMEs turn out to be fraudulent, a meaningful percentage at scale.

Without AML transaction monitoring layered with merchant risk monitoring, fraudulent merchants can collect settlements, disappear, and leave the acquirer absorbing the chargeback exposure.

This audience needs AML software integrated with merchant fraud detection, not just individual transaction screening.

Digital-first banks face a specific attack surface: Authorized Push Payment (APP) fraud, money mule networks, and account takeover (ATO) attacks. Fraudsters target neobank customers because onboarding is fast and monitoring is often weaker than at legacy banks.

AML software for this segment needs to monitor peer-to-peer transfers, flag mule account behavior, and detect coordinated fraud campaigns across account clusters - not just screen against a sanctions list at signup.

Card issuers manage both the customer-facing fraud risk (card-not-present fraud, account takeover) and the underlying AML obligation to monitor accounts for suspicious money movement. Issuers need real-time transaction monitoring that can flag unusual spending patterns, high-velocity activity, and counterparty risk, not just PEP screening at onboarding.

Many issuing processors resell their platforms to smaller issuers, making scalable, multi-tenant AML capability essential.

Companies processing cross-border transfers and remittances face some of the highest AML risk in the payments ecosystem.

High transaction volumes across multiple jurisdictions, mixed customer profiles, and strict data residency requirements in markets like the GCC, India, and Southeast Asia create a complex compliance environment.

AML software for this segment must handle volume at speed, support local regulatory reporting formats, and deploy within data sovereignty constraints.

Fraudio is the strongest AML platform on this list for payment-processing startups and fintechs. Based in Amsterdam, it serves issuers, acquirers, payment facilitators, fintechs, and processors across Europe, the Middle East, Southeast Asia, and beyond, with more than 2 billion transactions processed across 188 countries and over 1 million merchants across 548 industries.

Our AML product combines rules-based controls with AI-driven modeling and link analysis, so it supports both compliance operations and investigations in one system. That includes transaction monitoring, entity tracking, case management, SAR reporting, and sanctions and PEP data.

What really sets our platform apart is its patented centralized AI. Most AML platforms learn from one customer’s history, but Fraudio’s models learn from the combined data of every connected client while still keeping legal separation and data residency intact.

That means a newly onboarded fintech gets AI protection from the first transaction, backed by billions of events already in the model. Clients include Viva Wallet, Cashflows, Silverflow, and Pismo.

Fraudio’s main advantage is our network effect. When a startup connects, the platform immediately taps into pattern intelligence from billions of transactions across the whole client network, not just its own history, so fraud and money laundering signals learned from one client help protect every other client too.

It also deploys fast, in 3-14 days instead of 3-14 months. For a startup under regulatory pressure or racing a banking partner deadline, that speed can mean having working compliance controls in place on time instead of spending months in an integration project while exposure builds.

The pricing is built to be accessible; you pay only for transactions processed, costs per transaction fall as volume grows, and there are no setup, implementation, maintenance, or mandatory consulting fees, which makes total cost of ownership much more predictable.

Fraudio uses transparent, usage-based SaaS pricing with no setup, implementation, or maintenance fees. You only pay for transactions processed, and the per-transaction cost drops as volume grows.

For startups planning ahead, higher-volume commitments can unlock buy-rate pricing, which locks in a lower per-transaction cost for the full commitment term.

That gives faster-growing payment companies a more predictable, lower-cost structure as they scale, without changing the pay-per-use model.

For payment companies and fintech startups needing real-time AML that deploys in days, scales without proportional headcount growth, and brings network-level AI intelligence from the first transaction, Fraudio is the standout choice in 2026.

If you're a startup that processes payments and needs AML compliance that works from day one, this is where to start.

Flagright is also counted as one of the best AML software solutions for new startups, especially fintechs and financial institutions that need to go live fast without sacrificing compliance depth.

The platform covers the full AML compliance stack: real-time transaction monitoring, AML screening, dynamic risk scoring, case management, and SAR filing automation. Its ‘Startup Program’ is specifically designed for early-stage companies needing a fast, affordable AML foundation before they have a large compliance team.

Flagright also ranks on the RegTech100 for 3 consecutive years and has grown to serve customers across 6 continents.

Flagright is one of the stronger options for startups that are just getting started with AML compliance. The combination of fast deployment, no-code configuration, and a purpose-designed startup pricing program creates a genuinely accessible entry point that most AML vendors don't offer.

Flagright's Startup Program offers a 60% discount in Year 1 (all core features included, no long-term commitment), a 30% discount in Year 2, and standard volume-based pricing from Year 3 onward. Contact Flagright directly for current rates.

Flagright is one of the best AML software for startups requiring a working AML stack in weeks, not months. Such entities can’t usually commit to a large enterprise contract upfront, which is where the ‘Startup Program’ pricing comes in handy.

It is not the right fit if you also need payment fraud detection, merchant fraud monitoring, or deep centralized-AI capability beyond AML.

ComplyAdvantage is another great AML software for startup firms, founded in 2014. The company serves over 1,000 businesses across 75 countries and was recognized in G2’s ‘2026 Best Software Awards’.

Their platform uses proprietary AI to automate AML KYC screening, sanctions and PEP monitoring – along with adverse media checks and transaction risk management.

ComplyLaunch; their free access program for early-stage startups, has made them one of the most visible options for fintechs discovering AML compliance for the first time.

ComplyAdvantage is one of the best AML software for startups seeking entry points into structured AML screening for new startups.

Its ComplyLaunch program and low-entry ‘Starter’ pricing tier make it approachable at an early stage; and it's also amongst the more established brands in the space; something which matters when presenting compliance credentials to regulators or banking partners.

ComplyAdvantage restructured its pricing in 2026. The Starter Plan covers monitoring up to 2,000 entities and costs around $319/month.

The Enterprise Plan includes the full compliance platform with proprietary data, risk intelligence, and agentic AI workflows. At the enterprise scale, the pricing is custom and quote-based.

ComplyAdvantage is a smart first step for early-stage companies that need structured customer screening and sanctions monitoring, especially if the budget is tight.

For startups primarily focused on customer due diligence rather than real-time payment transaction monitoring at volume, it remains a strong contender.

SEON is a fraud prevention and AML compliance platform trusted by over 5,000 organizations globally, including Revolut and Wise. Founded in 2017 with offices in Austin, London, Budapest, and Singapore.

SEON's core differentiator is its 900+ first-party, real-time data signals covering email, phone, IP, device, and digital footprint data - layered with global AML watchlist data to build a unified fraud and AML workflow.

Unlike legacy providers that treat fraud and AML as separate functions, SEON integrates both into one real-time platform with a single API.

SEON is one of the best AML software solutions for companies looking to manage fraud prevention and AML within a single operational framework. Its high review scores on G2 and Capterra also reflect genuine user satisfaction, especially around ease of use and rule configurability.

SEON operates a tiered pricing model, with a free plan for testing up to 500 manual checks per month with 10 custom rules.

The Starter plan for SEON starts at €699/month with 1,000 API calls per month and 10 queries per second. More advanced tiers are available based on your use case, transaction volume and other specific factors. All plans are billed either monthly or annually.

SEON is a strong choice for mid-market companies that want unified fraud prevention and AML compliance without managing multiple vendor contracts. It is less suited to acquiring banks or payment facilitators that need deep merchant-level AML and fraud monitoring as part of their compliance stack.

Hawk is another top AML software solution for startups with AI-native AML and fraud prevention capabilities. The company was founded in 2018; and is headquartered in Munich, Germany.

Hawk's approach combines traditional rules-based AML controls with explainable AI, making it one of the stronger options for regulated financial institutions to demonstrate clear, auditable rationale for every automated decision – an increasingly important requirement under EU AMLA and US BSA regulations.

Hawk is one of the more thoughtfully built platforms in the AML space. Its explainability focus is not just marketing; and the company also has a patent pending for its approach. With an extensive customer base spanning top banks and payment providers in regulated markets, the company has solidified its position as one of the best AML software solutions for new startups.

Custom pricing based on institution size, selected modules, and deployment model. No publicly listed tiers. It's recommended that you contact their sales team for a quote.

Hawk is a strong contender for banks and established payment providers that need to modernize their AML compliance stack with explainable AI. For very early-stage startups or companies that primarily need customer screening, it may be more than needed at the initial stage.

Sardine is a San Francisco-based risk platform founded in 2020 by former Coinbase and Revolut risk executives. Their core differentiator is device intelligence and behavioral biometrics: it profiles how users physically interact with devices - typing patterns, swipe behavior, navigation speed, to detect account takeovers, APP scams, and synthetic identity fraud that transaction data alone doesn't surface.

Sardine serves over 300 enterprise customers including FIS, Deel, and GoDaddy, with over 5 billion devices profiled globally.

Sardine's combination of device intelligence, behavioral biometrics, and AML compliance in one platform is what makes them one of the best AML software for startups.

Most of these tools work from transaction data - Sardine adds the behavioral layer on top, which is particularly valuable for detecting socially engineered scams and money mule activity that look transactionally legitimate.

Sardine offers sales-led pricing with a minimum monthly commit drawn against usage. Their typical annual contracts are in mid-six figures depending on the modules and your requirements. It is recommended that you connect with their sales team for a custom quote.

Sardine is a compelling option for fintechs and digital banks facing high volumes of APP fraud, social engineering scams, and synthetic identity abuse. It is, however, not the right fit for acquirers or payment facilitators that primarily need merchant-level fraud monitoring and AML.

Feedzai is a global financial crime prevention company that risk-assesses approximately $9 trillion in payments annually across 120 billion events. Founded in 2011, it is an enterprise-grade AI platform that unifies fraud prevention and AML compliance for tier-one banks, large acquirers, and major payment processors.

In March 2026, Feedzai launched RiskFM - the industry's first tabular foundation model purpose-built for financial crime risk - representing a significant leap in model performance across fraud and AML detection.

Feedzai is one of the most technically sophisticated AML software for large financial institutions and enterprise banks requiring enterprise-grade fraud prevention and AML performance at scale.

For startups evaluating this list, Feedzai has been included for its completeness: the implementation timeline, cost structure, and technical complexity often make it an unsuitable choice at the early stage.

Feedzai offers custom enterprise pricing, with deployments for large financial institutions nearing mid-six figures. There are no publicly listed pricing tiers and costs are based on transaction volume, products deployed and institutional scope.

Feedzai is the right choice for large banks and enterprise processors that need a battle-tested, AI-native platform at scale. It is not suitable for startups or early-stage fintechs since the cost, complexity, and implementation timeline make it inaccessible and unnecessary at that stage.

NICE Actimize is the largest and most comprehensive provider of financial crime, risk, and compliance solutions for global financial institutions.

Serving over 1,000 organizations across 70 countries; it covers AML, enterprise fraud management, financial market compliance, trade surveillance, and investigation case management.

Their entity-centric approach positions the customer relationship; not the individual transaction; at the center of risk assessment.

NICE Actimize is one of the best AML software solutions for tier-one global banks and large financial institutions where regulatory breadth, modular complexity, and regulator-familiar tooling are non-negotiable requirements.

It is included on this list for completeness; for startups and growth-stage fintechs, the cost structure and implementation complexity make it an impractical starting point

Modular, custom pricing with no publicly listed pricing range. Usually involves significant capital, including implementation, module licensing and ongoing support fee.

NICE Actimize is a fit for the world's largest financial institutions where regulatory credibility, breadth of coverage, and modular complexity are requirements. For startups and growth-stage fintechs, the cost, complexity, and implementation timeline make it an impractical choice.

Salv is an Estonian AML compliance platform founded in 2018 by former TransferWise (now Wise) and Skype engineers.

It focuses on helping banks and fintechs move beyond traditional compliance approaches, combining screening, dynamic risk scoring, and transaction monitoring with its flagship Salv Bridge product, the world's first cross-border financial crime intelligence sharing network.

Salv Bridge has been adopted by major Nordic institutions including Swedbank and SEB.

Salv Bridge is one of the best AML software for startups, offering arguably the most innovative capabilities in the industry. No other vendor has operationalized cross-institutional financial crime intelligence sharing at this scale.

For banks and fintechs in markets where financial crime rings move across multiple institutions, this has genuine detection value that isolated systems can't replicate.

Custom pricing based on institution type, modules selected, and transaction volume.

Salv is a strong option for EU-based fintechs and banks that want modern AML compliance technology with a unique intelligence-sharing component. It is particularly valuable for organizations operating in markets where Salv Bridge has meaningful network penetration.

For companies outside the EU or those needing combined fraud + AML + merchant monitoring, other alternatives may provide broader coverage.

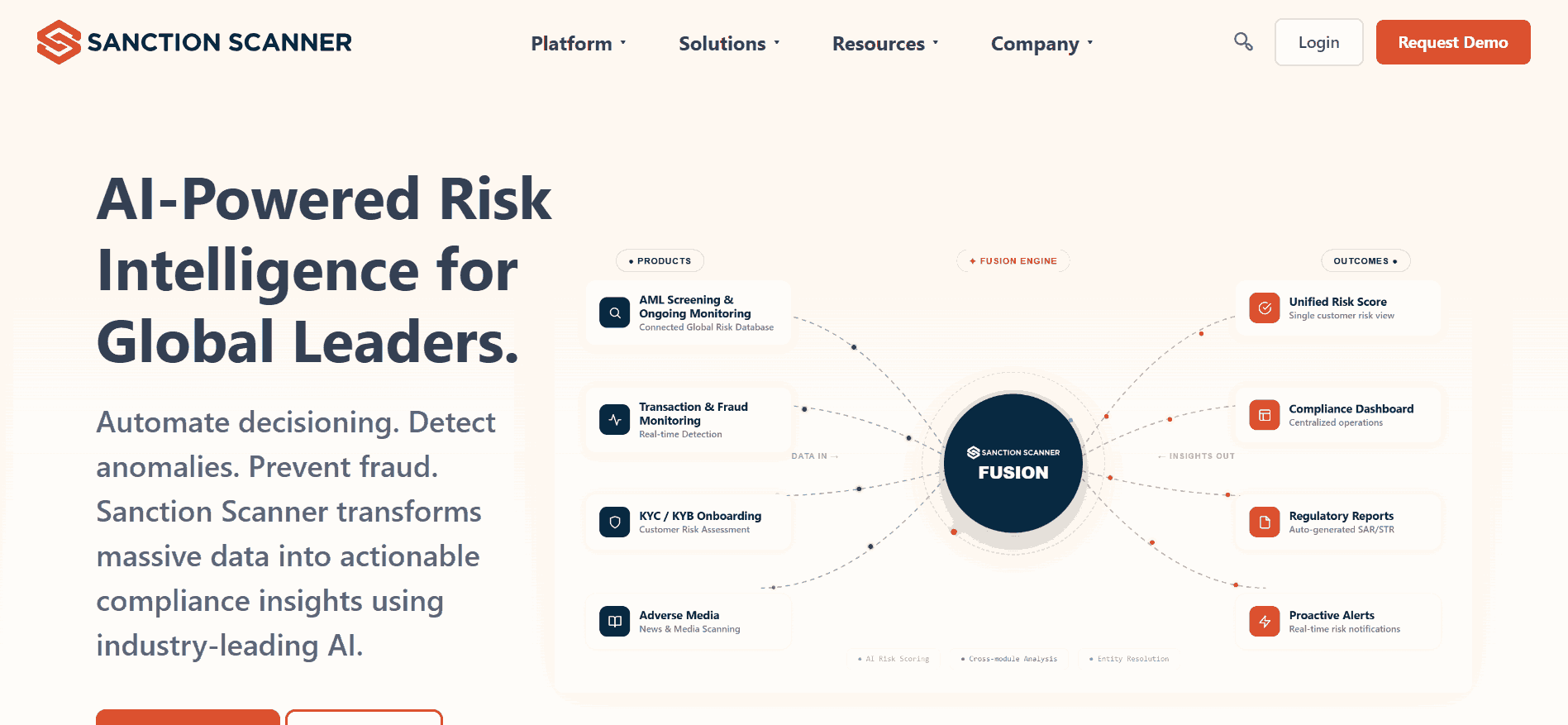

Sanction Scanner is a RegTech company providing AML name screening, transaction monitoring, and adverse media screening tools.

It serves compliance teams across financial services, banking, fintech, and regulated businesses that need to screen customers against global sanctions, PEP, and watchlist data with high accuracy and at low cost per check.

Sanction Scanner is one of the most accessible AML data tools for companies at the earliest stages of compliance buildout. Its per-check pricing means you pay for what you use, and the Excel batch option removes developer resources from the equation entirely.

They offer custom pricing based on your organization type, transaction volume and other similar factors. Recommend requesting a demo with the sales team on their website.

Sanction Scanner is a practical, cost-effective starting point for companies that need AML screening and watchlist coverage without the complexity or cost of a full compliance platform.

Best used as a screening data layer; either standalone at the earliest stage, or integrated alongside a transaction monitoring platform as compliance requirements grow.

Choosing the right AML platform early on is one of the highest-leverage decisions a payment startup can make. Get it right and you've got a compliance foundation that scales with you. Get it wrong and you're either re-platforming 18 months later or absorbing fines you didn't see coming.

Here's what actually matters.

This is the most important technical question to ask any AML vendor, and most startups never ask it.

Most AML platforms train their AI models only on a single customer's transaction history. For a startup processing a few million transactions a month, that means the model is learning from limited data, takes months to produce meaningful signals, and has no visibility into fraud and money laundering patterns occurring elsewhere in the market.

Fraudio's patented centralized AI is the structural exception: it learns from billions of transactions across all connected clients simultaneously, while maintaining full legal and data separation between them. A startup connecting to Fraudio gets network-level detection intelligence from the very first transaction - not after 18 months of model training on its own limited data.

Ask every vendor on your shortlist directly: does your AI train on my data only, or across a shared network? The answer tells you more about long-term detection quality than any feature comparison will.

If you have a regulatory review in 90 days, a banking partner requiring working compliance controls before they'll onboard you, or a card scheme audit approaching, deployment speed is not a feature to compare. It is a hard filter that eliminates most enterprise platforms before the evaluation begins.

Enterprise platforms require anywhere from 6 to 12 months from contract to first production deployment. Modern platforms built for startups operate on a completely different timeline: Fraudio deploys in 3 to 14 days, which for a startup under regulatory pressure isn't just convenient - it can be the difference between having compliant controls in place on time or not.

Know your deadline before you start evaluating features. A platform that can't have you live before your next compliance obligation isn't really an option.

Not all AML software covers the same ground. Some tools focus purely on customer screening, checking names against sanctions and PEP lists. Others add real-time transaction monitoring. Others go further into case management, SAR filing, and entity risk analysis across all payment types.

Before evaluating vendors, map out what your regulatory obligations actually require. A startup with an EMI license needs real-time transaction monitoring across cards, instant payments, APMs, and direct transfers - not just a name check at onboarding. Starting with the right scope prevents overspending on features you don't need, or underspending in ways that create compliance gaps down the line.

Most AML tools have pricing models that look affordable at first glance and become expensive quickly. Watch for setup fees, implementation fees, per-user licensing on top of transaction fees, mandatory consulting hours, and minimum transaction commitments.

Fraudio operates with zero setup fees and zero implementation fees, with the cost per transaction decreasing as volume grows. For startups where cost predictability matters, this pay-per-use model means you're not paying for scale you haven't reached yet. When comparing vendors, calculate the total cost of ownership over three years - not just the monthly line item.

If you're operating in or planning to expand into markets with strict data residency requirements - Saudi Arabia, UAE, India, or Indonesia - your AML vendor must be able to deploy infrastructure locally. Many can't.

This matters more for startups than it might seem. A platform that works well in Europe today but can't follow you into APAC, the Middle East, or LATAM 18 months from now forces a re-platform at the worst possible time. Fraudio currently serves clients across Europe, APAC, EMEA, and Latin America, and has proven local infrastructure deployments in five data residency-restricted territories: Europe, KSA, UAE, India, and Indonesia, with a track record of adding new data residency deployments within days.

If you're planning to expand internationally, verify a vendor's regional deployment capability before signing a contract, not after.

At the startup stage, your compliance team is probably small and may not have a dedicated AML analyst yet. AML software should make compliance easier, not require a specialist just to operate the dashboard.

Look for features like no-code rule builders, AI-assisted alert triage, and case management with built-in SAR reporting. When evaluating tools, test them with the actual person who will use the platform daily - not just the procurement team.

Fraudio's click-to-answer investigation environment is specifically designed so compliance teams can surface transaction data and build cases without routing requests through a data team.

Before signing any AML contract, confirm the platform can produce compliance outputs in the exact formats your regulators require. SAR formats differ between FinCEN (US), FIU (EU member states), FCA (UK), and local regulators in other markets. Some platforms support direct filing; others produce draft reports for manual submission.

If you're operating across multiple jurisdictions - or planning to - verify this before go-live. Discovering a reporting gap after you've launched is a costly and avoidable problem.

Most AML software was built for the enterprise procurement cycle: 12-month implementations, six-figure setup fees, and AI models that need 18 months of data before they produce useful signals. Fraudio is built for payment companies and fintechs that need compliance working now, not eventually.

Fraudio's patented centralized AI brings network-level intelligence from day one; trained across billions of transactions from every connected client simultaneously. When any client in the network catches a new fraud or money laundering pattern, every other connected client benefits instantly. That is a structural advantage no per-institution model can replicate.

The AML product covers the full compliance stack: transaction monitoring, entity tracking, sanctions and PEP data, case management, SAR reporting, and complete audit trails – in one integrated system, with pay-per-use pricing and no setup or implementation fees.

To see how Fraudio performs on your actual transaction data, request a Proof of Results test by submitting your historical data and receive a direct performance comparison against your current setup, with no commitment required.

The best AML software for startups in 2026 is Fraudio for payment companies and fintechs that process transactions, due to its pay-per-use pricing, 3–14 day deployment, and patented centralized AI that provides network-level detection intelligence from the very first transaction processed.

What should I consider when choosing the right AML software for my startup?

When choosing AML software, prioritize these factors: deployment speed against your actual compliance deadlines, pricing structure (watch for setup fees, implementation fees, and minimum commitments that inflate total cost of ownership), AI quality (ask whether the model trains on a shared network or only on your own limited transaction history), compliance scope (transaction monitoring and entity tracking, not just customer screening), data residency capability if you're operating in or expanding into restricted markets, ease of use for a small compliance team, and regulatory reporting compatibility for the exact formats your regulators require.

Fraudio differs from alternatives primarily through its patented centralized AI dataset, which pools transaction intelligence across all connected clients while maintaining full legal and data separation between them. Competitors' AI models typically train only on a single customer's isolated transaction history, limiting detection quality for newer or smaller clients.

Getting started with Fraudio begins with an integration kickoff call where the team walks through your infrastructure, data history, and compliance requirements. Technical integration via API typically completes within 3 to 14 days. Alternatively, you can start with a Proof of Results (PoR) test - submit historical transaction data, and the team will run Fraudio's AI against it to demonstrate performance improvement compared to your current setup, with zero commitment required upfront.

Switching to Fraudio is straightforward because the platform connects via standard API, batch, or webhook - compatible with virtually all modern payment infrastructure. The integration process typically takes 3 to 14 days. For companies on existing contracts with another vendor, Fraudio offers a Proof of Results (PoR) test that runs in parallel with your current setup using historical data, requiring minimal effort and zero commitment upfront.

Yes. Fraudio currently operates in Europe, Saudi Arabia (KSA), the UAE, India, and Indonesia - five territories with strict data residency requirements - and has proven the ability to add new data residency-constrained territories within days.

AML software is required for any fintech startup that processes financial transactions and holds a payment license, EMI license, or operates under banking regulations. Regulators including the FCA (UK), central banks across the EU, FinCEN (US), and equivalent authorities in APAC and the Middle East require transaction monitoring, customer screening, and suspicious activity reporting as baseline conditions of operation.

How about trying our solution and experiencing the next generation for yourself?