June 5, 2026

The best anti-money laundering software for fintech in 2026 has to do more than check a compliance box. It needs to detect real threats, reduce false positives, integrate fast, and scale with your business, without breaking the bank.

This guide covers 10 top-rated AML tools reviewed, with pricing, features, pros, cons, and a clear verdict on who each tool is right for.

AML software for fintech refers to the compliance technology that fintech companies use to detect, prevent, and report money laundering activity across their payment flows and customer accounts. Unlike traditional banks, fintechs scale fast; often onboarding thousands of customers a month through fully digital journeys, which means the compliance infrastructure needs to keep pace from day one.

The best anti-money laundering software for fintech is built for that reality: fast to deploy, able to handle high transaction volumes in real time, and smart enough to distinguish genuine risk from noise without a team of 50 analysts behind it.

The compliance bar is higher than most fintechs expect. EMI license holders carry the same AML obligations as traditional banks; transaction monitoring, SAR filing, sanctions screening, full audit trails and regulators across the EU, UK, and APAC are actively increasing enforcement.

According to Europol, only 1% of laundered money is ever intercepted globally, and that failure rate is exactly why regulatory bodies are pushing fintechs to move beyond basic rule engines toward AI-driven detection. Getting this wrong does not just mean a fine. For a growing fintech, a compliance failure can freeze operations, revoke licenses, and end the business entirely.

Fintechs occupy a uniquely exposed position in the financial crime landscape. Digital onboarding, instant payments, and cross-border transfers are the features that make fintech products attractive to customers; and exactly the same features that make them attractive to bad actors.

Fraudsters target platforms with fast, frictionless account opening because the window between onboarding and detection is widest there.

Without proper AML software fintech teams can actually act on, suspicious activity goes undetected until chargebacks arrive, regulatory audits begin, or card scheme monitoring programs come knocking.

The operational reality compounds the risk. Most fintech compliance teams are small, handling alert volumes that would challenge a team 3 times the size at a traditional bank. Legacy rule engines flood analysts with false positives; some institutions report false positive rates above 90%; leaving genuine money laundering patterns buried in noise.

This is why the best anti-money laundering software for fintech needs to do more than flag transactions: it needs to prioritize intelligently, surface patterns across accounts and time, and reduce manual review burden without sacrificing detection accuracy.

PayFacs and acquirers hold direct liability when a merchant on their platform engages in fraudulent or illegal activity.

Approximately 3% of new digitally-onboarded SMEs turn out to be fraudsters - a figure that becomes financially catastrophic at scale without automated detection. AML software helps identify suspicious merchant behavior, flag transaction laundering, and provide the audit trail regulators require.

Issuing banks and processors need AML tools that can monitor cardholder behavior across account-to-account transfers, cross-border payments, and unusual velocity patterns.

Regulatory frameworks including PSD2 and local central bank mandates require issuers to demonstrate ongoing transaction monitoring - not just at onboarding.

Digital-first banks attract heavy regulatory scrutiny precisely because they move fast and operate at scale. They need AML software that integrates via API, deploys in days, and doesn't require a compliance team of 50 to operate.

False positives that block legitimate transactions are also a serious problem for neobanks - customer experience and compliance must coexist.

Peer-to-peer and account-to-account payment flows carry elevated risk for money mule networks and authorized push payment (APP) fraud.

Wallet providers and remittance companies need monitoring that can track inflow-to-outflow ratios, counterparty relationships, and velocity anomalies in real time - not just batch processing at the end of day.

Fintechs applying for or upgrading EMI (Electronic Money Institution) licenses face AML requirements as a condition of approval.

As these companies grow, their existing rule-based systems or manual processes reach capacity long before their business does.

AML software for fintech is what bridges the gap between startup compliance and institutional-grade monitoring.

Fraudio is a fraud and AML prevention platform built specifically for payment companies. Headquartered in Amsterdam and trusted by organizations like Viva Wallet, Cashflows, Silverflow, and Pismo, our AML product combines rules-based controls with AI-driven modeling across a patented centralized dataset, processing over 2 billion transactions across 188 countries.

Unlike most AML tools that train AI models only on a single customer's data, our centralized AI learns from billions of transactions across our entire customer network in real time. That creates a network effect: the more customers connected, the more accurate the detection for everyone. For fintech companies and payment processors who need both AML compliance and real-time fraud detection in a single, fast-to-deploy tool, we are the most capable option on this list.

We have 4 core products: Payment Fraud Detection (PFD), Merchant Initiated Fraud Detection (MIF), AML, and Peer-to-Peer Transfer Monitoring (P2P); each purpose-built for specific risk vectors within the payments ecosystem.

Most of the top anti-money laundering tools for fintech train on isolated, single customer data. Fraudio's patented centralized dataset breaks that limitation: models see patterns across billions of transactions from multiple issuers, acquirers, and payment types simultaneously.

Our customers usually detect merchant fraud 3 weeks earlier than their previous legacy system. We’ve also helped them increase their fraud team’s efficiency by 600%, while improving transaction volume by 7x without increasing additional compliance headcount.

Fraudio operates a transparent, pay-per-use pricing model. There are no setup fees, no implementation fees, no maintenance fees, and no mandatory consulting charges.

You pay only for the transactions processed, and the per-transaction cost decreases as your volume increases. For organizations committing to higher volumes, buy-rate options are available to lock in lower per-transaction pricing for the contract term.

This model makes Fraudio accessible to both emerging fintechs processing millions of transactions monthly and large processors running billions.

For fintech companies and payment processors looking for the best anti-money laundering software that also handles real-time fraud detection, Fraudio is the top anti-money laundering tool for fintech.

Our patented centralized AI, rapid deployment, and pay-per-use pricing model address the 3 biggest problems in this market: accuracy, speed, and cost.

ComplyAdvantage is a London-based financial crime intelligence company offering AML/KYC screening, transaction monitoring, and sanctions/PEP data across 75 countries. Their Mesh platform pairs proprietary global risk data with AI-native risk scoring, and their 2026 release introduces agentic workflow capabilities that automate a significant portion of routine alert resolution.

ComplyAdvantage is particularly strong for cloud-native fintechs requiring real-time sanctions screening, adverse media detection and automated risk assessment. This makes them one of the best anti-money laundering software for fintech companies handling cross-border payments.

ComplyAdvantage is one of the strongest choices for organizations that prioritize data quality and speed in global screening. Their AI-native approach to customer monitoring - continuously profiling risk across a broad set of global sources - is among the most advanced in the mid-market AML space. The company earned a spot on G2's 2026 Best GRC Products list (#28) and has expanded into agentic AI workflows for compliance automation.

ComplyAdvantage offers a Starter Plan from $319/month (billed annually) for monitoring up to 2000 monitored entities, with core screening and monitoring tools included.

Enterprise plans with full access to the proprietary data platform, agentic AI workflows, and real-time screening capabilities are available on custom pricing. Contact their sales team for a quote.

ComplyAdvantage is amongst the top anti-money laundering tools for fintech companies that need world-class sanctions screening, PEP monitoring and automated customer risk profiling.

SEON is an AML compliance and fraud prevention platform that focuses on digital footprint analysis, device intelligence, and transparent machine learning.

Trusted by over 5,000 customers, SEON is one of the top anti-money laundering tools for fintech that combines onboarding risk checks with ongoing transaction monitoring in a single API-first interface.

SEON is particularly popular with mid-market fintechs, iGaming companies, and payment providers that need fast, flexible fraud and AML checks; particularly at the customer onboarding stage.

SEON is one of the fastest and most accessible platforms in the top anti-money laundering tools for fintech category. The 14-day average deployment, the $0 free tier for manual checks, and the transparent tiered pricing make it feasible for companies at an early growth stage.

Their AI tools cut manual review time by up to 50%, according to their own data, and the whitebox machine learning model is valuable for teams that need to explain decisions to regulators.

The Starter plan for SEON starts at €599/month with 1,000 API calls per month and 10 queries per second. Growth and Enterprise tiers are available on custom pricing. All plans are billed monthly or annually.

SEON is one of the best anti-money laundering software for fintech companies in the mid-market space. These companies usually need fast AML screening and fraud detection at the onboarding layer.

That being said, it's not the right tool if you're processing billions of transactions and need deep real-time payment-level monitoring with network-effect AI.

Feedzai is an AI-native platform that unifies fraud detection, AML, and customer lifecycle management under a single RiskOps framework. The company claims to protect $8 trillion in transactions annually and serves major banks and payment service providers globally.

Feedzai's strength lies in combining adaptive AI with user-defined rules and robust case management for enterprise-scale institutions.

Feedzai is one of the best AML software for fintech organizations at the enterprise level. These companies usually need comprehensive coverage across the entire financial crime spectrum.

Feedzai’s AI-native design, without legacy constraints, and its ability to handle global-scale transaction volumes make their solution apt for large banks and processors.

The platform's focus on ‘Responsible AI’ - with explainability built in, is also relevant for institutions facing increasing scrutiny over the transparency of their automated decisions.

Feedzai uses custom enterprise pricing. There are no publicly listed tiers. The price you pay is based on transaction volume, products deployed, and institutional scope. You can expect a significant capital commitment typical of enterprise B2B software.

Feedzai is one of the most capable platforms on this list for large financial institutions that want a single vendor covering fraud, AML, and risk management.

The challenge for most fintech companies is the enterprise orientation - if you're not already processing at tier-one bank volumes, the cost and deployment timeline will outweigh the benefits.

NICE Actimize is a veteran enterprise platform covering fraud prevention, AML, suspicious activity monitoring, and trade surveillance. Founded in 1999 and acquired by NICE Ltd in 2007, it remains one of the benchmark tools for large global banks managing complex multi-jurisdictional compliance.

Their entity-centric approach positions the customer relationship; not the individual transaction; at the center of risk assessment.

NICE Actimize has decades of proven track record at the most demanding compliance environments globally: tier-one banks, global financial institutions, and regulatory bodies where the cost of a false negative is an enforcement action.

Its modular suite allows large organizations to manage every facet of financial crime prevention from a single vendor.

For most fintech companies, it is included on this list for completeness: the cost, complexity, and deployment timelines make it an impractical choice outside of major global financial institutions.

NICE Actimize uses custom enterprise pricing available only through a direct sales engagement and there are no publicly listed tiers. This usually involves significant capital investment – including implementation fees, module licensing and ongoing support costs.

NICE Actimize is one of the top anti-money laundering tools for fintech companies that need proven, enterprise-grade infrastructure. These companies usually have a high budget and the required internal resources for a successful implementation.

If you are not a major global bank; the cost, complexity, and deployment timelines will create more problems than the platform solves.

Napier AI is a London-based AML compliance platform focused on making enterprise-grade monitoring more accessible, explainable, and user-friendly than legacy alternatives. Their Continuum platform integrates transaction monitoring, client screening, and case management into a single dashboard, with a cloud-native, API-first architecture.

Napier is particularly notable for its "overlay" model - the platform can sit on top of existing legacy systems to enhance detection without requiring a full rip-and-replace.

Napier AI is the best anti-money laundering software for fintech companies caught between the expense of enterprise platforms like NICE Actimize and the limitations of a basic, rule-based tool.

The explainable AI is particularly compelling for UK institutions subject to NCA scrutiny, where SAR narrative quality can be a regulatory differentiator. In addition, the overlay architecture also means existing data investments don't go to waste.

Napier AI pricing is custom and available through direct contact/request placed with their sales team. You can get a customized plan based on the required AML features and support, add-ons and bespoke deployment options.

Napier AI is a well-designed platform for mid-market compliance teams seeking modern tooling without enterprise-tier costs or deployment complexity. The explainable AI and sandbox testing are genuine differentiators.

Where Napier falls short is in deep, real-time payment processing scenarios at issuer or acquirer scale - for that workload, the network-effect AI and dual-rail architecture of a purpose-built payments platform like Fraudio is a better option.

Quantexa is a Decision Intelligence company that approaches financial crime through graph-based network analysis. Rather than analyzing transactions in isolation, Quantexa maps relationships across entities, accounts, and data sources to uncover hidden networks that conventional monitoring misses.

Quantexa is particularly effective for complex corporate structures, correspondent banking and trade finance scenarios where layered ownership obscures the source of funds.

Quantexa's graph-based approach is among the most sophisticated financial crime detection methodologies available. For institutions managing complex multi-entity corporate relationships or investigating sophisticated laundering operations, the ability to visualize and analyze entire financial networks represents a fundamentally different level of detection capability.

Quantexa uses custom enterprise pricing, with no public tiers advertised on their website. Their pricing plans usually reflect the scale of data infrastructure, number of entities modeled, and deployment scope.

Quantexa is a compelling choice for data-rich and analytically sophisticated institutions (such as global banks) managing thousands of complex corporate relationships or financial crime investigations.

For most fintech companies, the complexity, cost, and technical requirements are disproportionate to the use case. Simpler, faster-to-deploy platforms will deliver better value.

SAS Anti-Money Laundering is built on SAS's decades-long foundation in analytics and data science.

The platform provides end-to-end AML coverage: transaction monitoring, watchlist screening, case management, and regulatory reporting – with special focus on allowing technically sophisticated compliance teams to build and tune their own detection models.

SAS brings unmatched analytical depth to AML compliance. For institutions with in-house data science capability, the ability to build, test, and deploy custom detection models on top of SAS's analytics engine is a significant competitive advantage.

No other platform in this comparison offers the same level of model transparency and customizability for technically capable teams.

SAS Anti-Money Laundering uses custom enterprise pricing reflecting the complexity of each deployment. There are no publicly listed tiers. Contact SAS directly for a quote based on your transaction volume, user count, and required analytics capabilities.

SAS AML is a great choice for technically mature financial institutions that want maximum analytical customizability and have the data science talent to exploit it.

For most fintech companies, particularly those prioritizing speed, simplicity, and cost efficiency; the technical overhead and enterprise pricing of SAS will outweigh its analytical advantages.

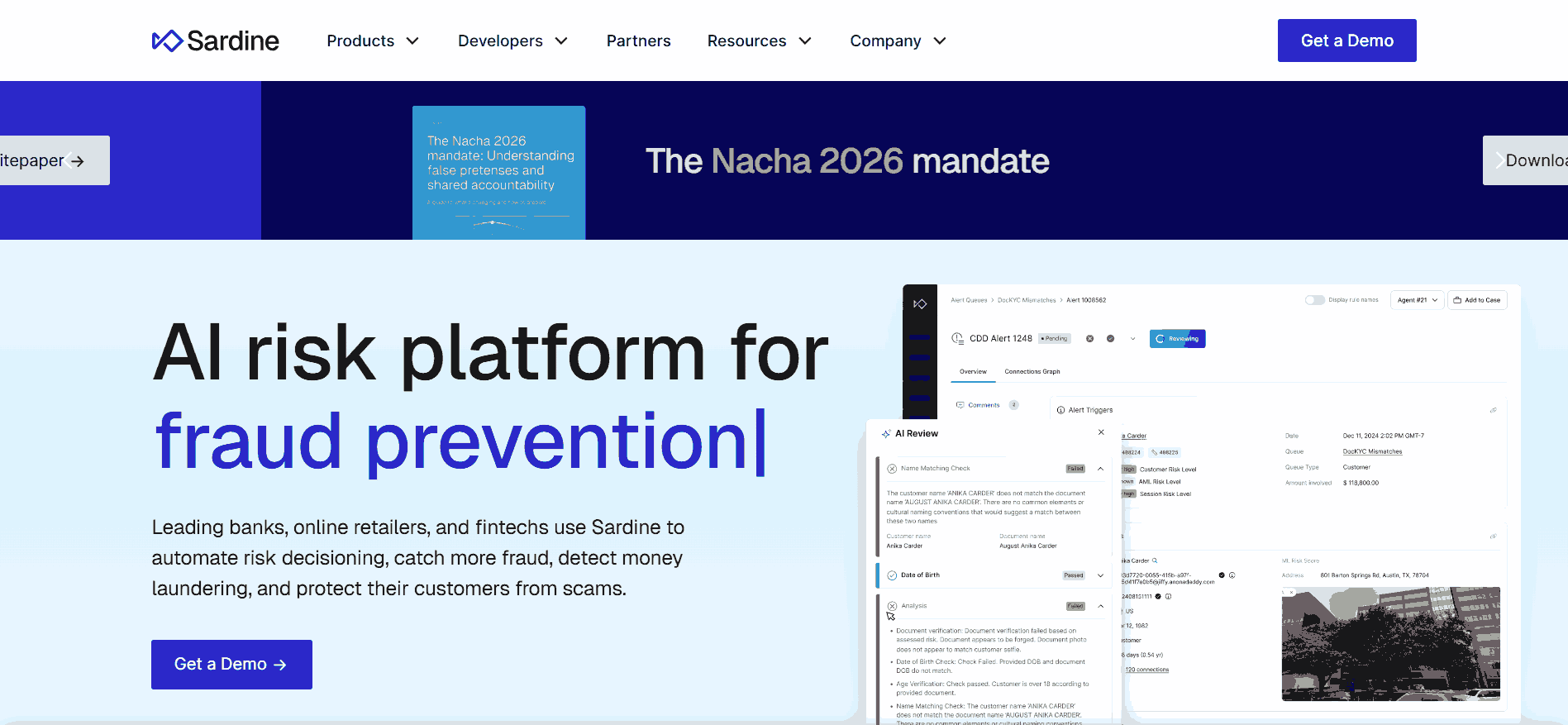

Sardine is a fraud and compliance platform that originated in the neobank and fintech space. It specializes in device intelligence, behavior biometrics, and fast onboarding risk decisions - with sub-50ms decision speed and a database of 2.2 billion profiled devices.

Sardine has particular strength in crypto, digital wallets, and fintechs that need to assess risk at the moment of account opening, not just at the payment layer.

Sardine is one of the strongest choices for fintech companies where device-level intelligence and behavioral signals are a primary risk layer. The sub-50ms decision speed is genuinely differentiated, and the 2.2 billion device database creates network effects at the onboarding layer.

For crypto companies and digital-first fintechs that see large volumes of new account creation, Sardine addresses fraud earlier in the funnel than most AML tools.

Sardine uses custom pricing and you must contact their sales team for a customized plan based on your transaction volume, product mix, and company profile.

Sardine is a top-tier choice for digital-first fintechs, crypto platforms, and neobanks where the risk surface is concentrated at account opening and the first few transactions.

Fraud.net is a risk management platform offering joint AML and fraud transaction monitoring in a single interface. Recognized with the ‘2024 Datos Insights Award’ for its Joint AML and Fraud Transaction Monitoring solution, Fraud.net serves fast-scaling B2B organizations that want entity-first risk monitoring with no-code decisioning capabilities and flexible API integration.

Fraud.net's joint AML and fraud monitoring approach reduces toolchain complexity for compliance teams. The no-code rule engine and flexible data orchestration make it particularly accessible for B2B fintech companies that don't have large engineering resources dedicated to compliance infrastructure.

Fraud.net uses custom pricing. Contact their sales team directly to get a quote tailored to your transaction volume and product requirements.

Fraud.net is a solid option for B2B fintech companies that want consolidated fraud and AML coverage without managing two separate vendor relationships.

It’s one of the best anti-money laundering platforms for fintech organizations in the mid-market growth stage. Such companies usually prioritize solutions with toolchain simplicity that delivers real operational value.

Here’s everything you need to choose the best AML software for your fintech organization:

This is the most important technical question to ask any AML vendor, and most fintech buyers never ask it.

Most AML platforms train their machine learning models only on a single customer's transaction history. For a fintech processing a few million transactions a month, that means the model is learning from limited data, takes months to produce reliable signals, and has no visibility into fraud and money laundering patterns occurring elsewhere in the market.

Our patented centralized AI is the structural exception: it learns from billions of transactions across all connected clients simultaneously, while maintaining full legal and data separation between them.

A fintech connecting to Fraudio gets network-level detection intelligence from the very first transaction; not after months of model training on its own limited history.

Ask every vendor on your shortlist directly: does your AI train on my data only, or across a shared network? The answer tells you more about long-term detection quality than any feature comparison will.

Not all AML software detects the same things. Tools like ComplyAdvantage excel at customer screening - sanctions lists, PEP checks, adverse media; but are not purpose-built for monitoring millions of payment transactions per day.

Platforms like Fraudio or Feedzai are built for payment-level transaction monitoring at scale.

Map your risk surface before evaluating tools: if your primary concern is monitoring ongoing transactions from merchants or customers, you need a different tool than if your main concern is onboarding screening.

Compliance timelines are rarely forgiving. If you've received a regulatory notice, if you're applying for an EMI license, or if your current tool is failing - you probably can't wait 6–12 months for implementation.

Ask every vendor: what is the median time from contract signature to live deployment?

For context, Fraudio deploys in 3–14 days whereas other ‘Gen 2’ enterprise platforms require 5–14 months.

If you operate in KSA, UAE, India, Indonesia, or other data-residency-restricted territories, confirm that any vendor you're evaluating can actually host your data in those regions.

Several well-known platforms simply cannot deploy in certain jurisdictions. Fraudio is currently live across all five data-residency-restricted territories mentioned above.

Published pricing is rarely the full picture. Watch for setup fees (often $50,000–$250,000 for enterprise platforms), implementation consulting (billed at day rates), annual license minimums, and per-rule charges.

Fraudio's pay-per-use model with no setup fees is an explicit response to this problem, but any vendor conversation should include a total cost of ownership calculation, not just monthly pricing.

A system that flags everything detects everything - but also creates an investigation backlog that overwhelms your compliance team.

Ask vendors for their false positive rate data, request a Proof of Results (PoR) test using your historical transaction data before committing, and evaluate how tunable the model is post-deployment.

Detection is only half the job. Your compliance team still needs to investigate alerts, document findings, and file SARs. Evaluate the case management interface carefully - how many clicks does it take to move from alert to filed report?

Does the tool generate SAR-format outputs directly? Fraudio's built-in case management with direct SAR download is designed to reduce this friction significantly.

AML regulations differ materially across markets. PSD2 in Europe, FinCEN in the US, MAS guidelines in Singapore, and local central bank requirements in markets like Indonesia and Saudi Arabia all have specific technical requirements.

Confirm that your chosen platform has been deployed and verified compliant in every market you operate in - not just that it's "globally compatible" in a marketing sense.

If you're looking for the best anti-money laundering software for fintech in 2026 - something that deploys in days rather than months, costs less than enterprise incumbents, and gives you AI that learns from network-wide data rather than just your own transaction history - we're built for exactly that.

Our AML product combines rule-based controls with centralized AI modeling across billions of transactions. It includes full case management, SAR-format reporting, sanctions screening, entity tracking, and full audit trails.

When any client in our network identifies a new fraud or money laundering pattern, every other connected client benefits instantly. That is a structural advantage no per-institution model can replicate, and it is active from your very first transaction.

One of our clients, Viva Wallet – achieved 8x ROI and 600% increase in fraud team efficiency within a deployment that completed in days.

To see what our AI catches on your transaction data, request a Proof of Results test – no commitment required.

The best anti-money laundering software for fintech in 2026 is Fraudio. It is an ideal solution for any payment company that needs real-time transaction monitoring combined with AI-driven detection at scale. Our patented centralized AI learns from billions of transactions across its entire customer network, delivering network-effect detection accuracy that siloed tools cannot match.

When choosing AML software for fintech, the 5 most important factors are: detection accuracy (AI quality and data depth), integration speed, total cost of ownership (setup fees, implementation costs, and per-transaction pricing all compound), data residency support, and case management quality. It’s recommended that you request a ‘Proof of Results’ test using historical data before you commit to a contract/subscription.

Fraudio differs from alternatives through its patented Network Effect AI. While competitors operate with siloed AI models that learn only from each individual customer's transaction history, our AI trains on a centralized dataset from across our entire customer network - covering billions of transactions from issuers, acquirers, payment facilitators, and more simultaneously. This delivers detection accuracy from day one, without the 3-6 month ramp-up period that siloed models require.

Getting started with Fraudio begins with an integration kickoff call where our team walks through your infrastructure, data history, and compliance requirements. Technical integration via API typically completes within 3 to 14 days. If you want to see results before committing, we offer a Proof of Results (PoR) test; submit your historical transaction data and our team will run our AI against it to demonstrate performance improvement compared to your current setup, with zero commitment required.

Switching to Fraudio is straightforward. If you're mid-contract with another tool, we run a Proof of Results test in parallel using your historical data; no integration, no commitment, just a clear view of what our AI catches that your current system misses. Once you're ready to move, our API-first architecture connects in days, rule libraries give immediate baseline coverage, while

the centralized AI adapts to your transaction patterns from thereon.

For KYC/KYB checks, PEP screening, adverse media monitoring, and device intelligence, we work with a curated partner ecosystem; integrating best-of-breed providers rather than building a diluted version of each capability in-house. This means your KYC/KYB data can feed directly into Fraudio's transaction logic, enriching the AML detection layer with identity-level context.

AI-based transaction monitoring isn't universally mandated by name, but regulators are effectively requiring it in practice. The EU's AMLA framework, operational since mid-2025, sets standards that manual rule engines struggle to meet at scale. FinCEN's expanded AML/CFT rules push US investment advisers toward automation, and FATF recommendations increasingly reference technology-enhanced monitoring as a baseline expectation.

How about trying our solution and experiencing the next generation for yourself?