June 5, 2026

Kount, now part of Equifax following its 2021 acquisition, is a well-established fraud prevention platform with a long track record in the eCommerce space. Its Identity Trust Network combines device, behavioral, and identity signals to help merchants reduce chargebacks, detect account takeovers, and manage authorization fraud.

Kount Command and Kount Central both offer rules-based and ML-driven controls with relatively broad coverage for merchant fraud use cases.

For companies already in the Equifax ecosystem, the integration path is straightforward and the combined data signals can be meaningful.

Kount also offers both cloud and on-premises deployment options, which matters for organizations with data residency requirements.

Despite its strengths, Kount pushes many teams to look for Kount alternatives for several recurring reasons:

These gaps are precisely what the best Kount competitors on this list address.

We built Fraudio as a next-generation fraud and AML prevention platform for payment companies that need real-time detection without the cost, complexity, and long integration timelines of legacy enterprise tools.

Our patented centralized AI technology is the core differentiator among all best Kount alternatives on this list: rather than training models in isolation on each customer's own data, our system centralizes transaction data across all connected customers into a single dataset. Models learn from billions of transactions in real time, meaning every new customer benefits from fraud patterns detected across the entire network from day one.

This network effect matters practically. When we detect a new fraud typology at a payment facilitator in APAC, that pattern is immediately available to every other connected customer, including an issuer in Europe or an acquirer in LATAM. Legacy tools, including Kount, cannot do this because their models are siloed per customer.

We offer four core products covering the full payment fraud and compliance landscape: Payment Fraud Detection (PFD) for real-time transaction scoring, Merchant Initiated Fraud Detection (MIF) for catching fraudulent merchants before settlement, AML transaction monitoring, and P2P Transfer Monitoring for instant payment and wallet providers. All four run on the same underlying centralized AI infrastructure.

Fraudio integrates in 3 to 14 days versus the 5 to 14 months typical for Gen 2 platforms. The results we got for Viva Wallet is our clearest proof point: 8x ROI, 600% increase in fraud team efficiency, and fraud caught 3 weeks earlier than their legacy tools, all achieved within weeks of deployment. We are also deployed at Cashflows, Silverflow, Pismo, Paynovate, and Paymentology, among others – payment companies across issuing, acquiring, and processing in Europe, APAC, and LATAM.

In addition, our platform is ISO27001-certified, fully GDPR & PSD2 compliant and deployed in data residency-restricted territories including: Europe, KSA, UAE, India and Indonesia.

Kount's AI learns only from its own customers' data, and its product coverage is primarily focused on transaction-level card fraud for merchants.

We cover four fraud vectors in a single platform, our AI learns from the entire network rather than isolated customer data, and we integrate in days rather than months.

For payment companies that have outgrown rule-based systems but cannot justify Kount's enterprise pricing and timeline, we deliver measurable ROI immediately, not after a 12-month implementation.

The Viva Wallet result, 8x ROI with 600% fraud team efficiency improvement, is not a projection, but a live deployment result – making us one of the best Kount alternatives in the market.

Fraudio operates a pay-per-use SaaS pricing model. Customers pay per transaction processed; the cost per transaction decreases as volume grows. No setup fees, no implementation fees, no maintenance fees, and no hidden charges.

Customers can commit to higher volumes to lock in buy rates. Exact pricing is available through direct contact with the sales team.

A Proof of Results (PoR) test using historical data is available before committing to a full deployment.

Fraudio is the best Kount alternative for any payment company that needs real-time fraud detection and AML that works from day one, scales without enterprise-level friction, and covers more fraud vectors than Kount in a single integrated deployment.

If you are an acquirer, payment facilitator, or issuer outgrowing internal rules and looking for AI that learns from the entire payments network, not just your own data, we deliver that at a cost structure that makes it accessible from day one.

SEON is one of the best Kount competitors for digital-first businesses that prioritize deployment speed and pricing transparency. Founded in 2017 in Budapest, SEON targets mid-market fraud teams that want real-time risk scoring without a months-long integration project.

Their fraud detection platform aggregates over 900 first-party signals across email, phone number, IP address, device fingerprint, and behavioral data to build user risk profiles from the first interaction. SEON's pricing transparency is unusual in the fraud detection category; published tiers starting at $699/month make it accessible for teams comparing total cost of ownership without a lengthy sales process.

SEON integrates in as little as 14 days via a single API and covers both fraud detection and AML sanctions screening, making it a reasonably complete solution for companies that need to address multiple compliance requirements without building a multi-vendor stack.

For teams researching best Kount alternatives on a budget with a tight deployment window, SEON consistently ranks as one of the most practical starting points.

SEON addresses two of the most common complaints about Kount: opaque pricing and slow deployment. Published starting pricing (at $699/month) and a 30-day trial on paid tiers reduce the commitment required to evaluate the platform.

The API-first design means teams with developer resources can evaluate and go live faster than with any enterprise incumbent.

SEON's paid plans start at $699/month, covering core fraud detection and digital footprint enrichment.

A free plan is available for smaller teams. A 30-day free trial is offered on paid tiers. Enterprise and professional plans with expanded limits are available on request.

SEON is one of the best Kount alternatives for digital-first companies and fintechs that need fast deployment and pricing transparency.

For payment companies needing deeper merchant fraud detection, AML case management, or network effect AI drawing on cross-industry transaction data, a more specialized platform would provide more complete coverage.

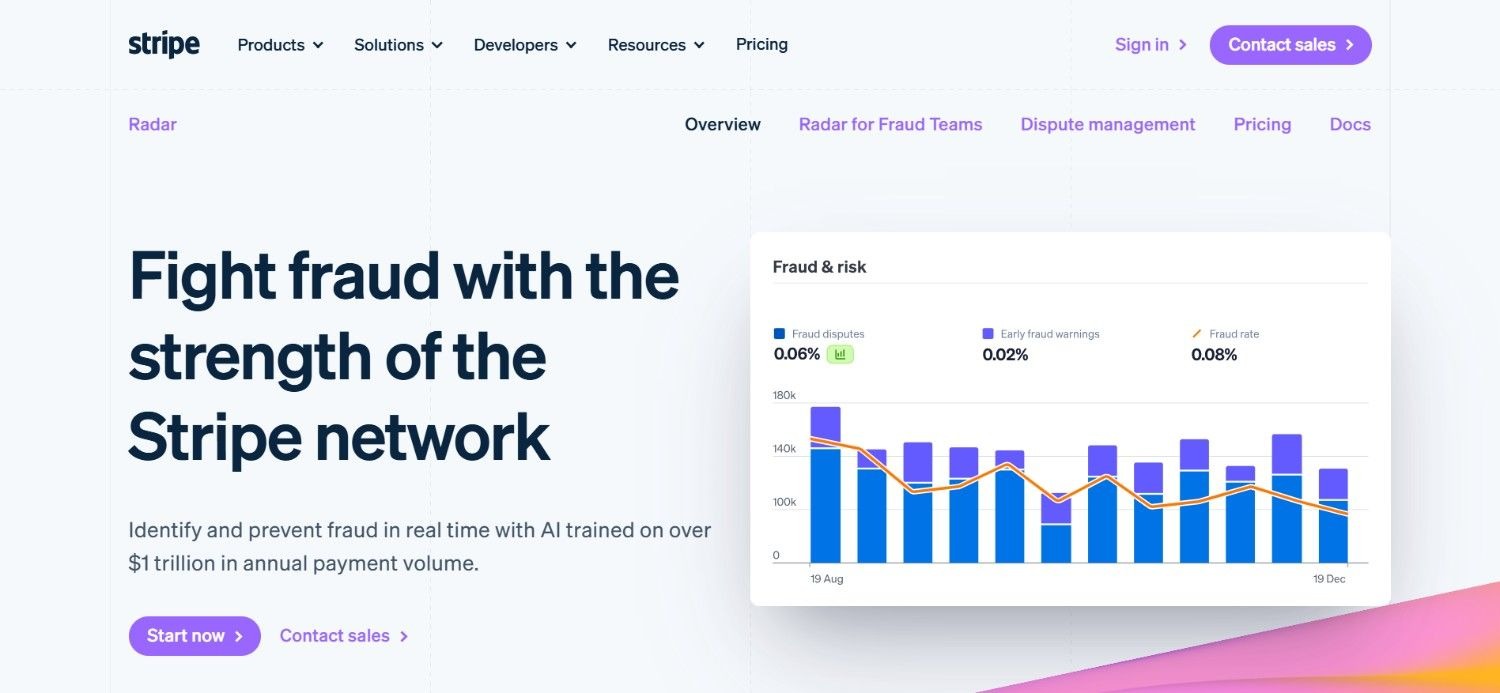

Stripe Radar is the fraud detection layer built directly into Stripe's payment processing network. It uses machine learning trained on Stripe's global transaction data, covering billions of payments across millions of businesses, to score transactions at the point of authorization.

For businesses already processing payments on Stripe, Radar requires no separate integration: the ML scoring is active by default, and the Radar for Fraud Teams tier adds custom rules, advanced dashboards, and granular fraud controls.

The combination of network-level training data and zero additional integration makes Stripe Radar one of the most accessible Kount alternatives for Stripe-native eCommerce businesses. That said, Stripe Radar's value proposition is inseparable from Stripe's payment network.

It only applies if Stripe is your payment processor; organizations that process through other acquirers cannot use it, and its scope is limited to transaction-level card fraud rather than the broader fraud vectors (merchant fraud, AML, P2P) that some payment companies require.

For Stripe-native businesses, Radar eliminates the integration overhead that makes most fraud tools challenging to deploy.

The per-transaction pricing model is straightforward and the ML quality benefit from Stripe's network data is genuine.

Stripe Radar's ML-based fraud detection is priced at €0.05 per screened transaction. The Radar for Fraud Teams plan, which adds custom rules and advanced dashboards, is €0.07 per screened transaction.

Enterprise and high-volume custom pricing is available through Stripe's sales team.

Stripe Radar is one of the top picks for businesses already processing on Stripe who want fraud coverage without a separate integration project.

For organizations that process through multiple acquirers, need merchant fraud detection, AML monitoring, or operate outside the Stripe ecosystem, a dedicated fraud platform will be necessary.

Microblink occupies a distinct position in the best Kount alternatives landscape: rather than transaction monitoring or behavioral fraud scoring, Microblink focuses on document-based identity verification and biometric authentication.

Their core products, BlinkCard and BlinkID Verify, use AI-powered document scanning and liveness detection to verify government-issued IDs, prevent synthetic identity fraud, and detect deepfake documents during onboarding. During independent testing validated by the U.S. Department of Homeland Security against the most extensive public deepfake dataset, Microblink recorded 100% deepfake detection accuracy.

Microblink fits the “best Kount alternatives" conversation because Kount users often cite identity verification capabilities as a reason they are evaluating alternatives. However, it is worth being clear: Microblink is a specialized identity verification tool, not a real-time transaction monitoring platform.

Teams that need onboarding fraud prevention alongside transaction scoring will need to pair Microblink with a transaction monitoring platform.

For teams evaluating the best Kount alternatives specifically because of identity verification gaps at onboarding, Microblink is a purpose-built replacement for that capability.

The deepfake detection track record in particular addresses a fraud vector that most general-purpose fraud tools do not cover with the same depth.

Microblink uses custom pricing based on verification volume, deployment requirements, and the specific products required. Contact their sales team directly for a tailored quote.

Microblink is one of the best Kount alternative for organizations whose primary pain with Kount is identity verification quality at onboarding, particularly for deepfake and synthetic identity fraud.

For teams that also need ongoing transaction monitoring, AML, or merchant fraud detection, Microblink would need to be paired with a transaction-level fraud platform.

Signifyd is a fraud protection platform built specifically for eCommerce, known for its financial guarantee model: Signifyd absorbs the chargeback liability on orders it approves, giving merchants direct financial protection against fraud losses rather than just risk scores.

Their ‘Commerce Protection’ offering covers fraud prevention, account abuse, policy abuse, and payment compliance in one product.

As one of the more popular Kount alternatives among eCommerce retailers, Signifyd has built a following among large merchants that want to reduce false declines without carrying residual chargeback risk on approved orders.

Counted amongst the best Kount competitors for eCommerce merchants, Signifyd's guarantee model is genuinely differentiated: rather than improving fraud scores, it removes the financial exposure entirely on covered orders.

Signifyd's guarantee model is the clearest differentiator in the eCommerce fraud space and a key reason it comes up frequently when merchants compare best Kount competitors.

For merchants who are tired of managing risk score thresholds and want the liability moved off their balance sheet, this is a compelling model. The network effect from Signifyd's merchant coverage provides meaningful signal quality for consumer-facing eCommerce use cases.

Signifyd offers custom pricing. Contact their sales team to receive a tailored plan based on transaction volumes, order mix, and chargeback protection requirements.

Signifyd is one of the best Kount alternatives for eCommerce merchants that want to eliminate chargeback liability rather than manage fraud scores.

For payment processors, acquirers, and fintechs that need broader transaction fraud coverage, AML, or merchant fraud detection, Signifyd's eCommerce focus limits its applicability.

Sift is a fraud platform known as a "Digital Trust and Safety" provider, covering fraud across the full customer lifecycle rather than focusing solely on payment authorization. Their product suite covers payment fraud, account fraud, account takeover, content abuse, and dispute management.

Sift builds behavioral profiles for users across the customer journey, using signals from account creation through transaction completion to identify anomalous patterns that indicate fraud rather than just evaluating individual payment events.

Among the best Kount alternatives, Sift stands out for its account fraud and account takeover coverage, which complements its transaction fraud capabilities and makes it more relevant for businesses where account-level fraud is as significant as payment fraud.

Sift's behavioral analysis across the full customer journey is meaningfully deeper than Kount's transaction-event-focused approach for companies where account-level fraud is a primary concern.

The case management and analyst workflow tooling is also more mature than many competitors.

Sift offers custom, usage-based pricing. Packages are based on transaction volume, feature set, and platform usage frequency. Contact their sales team for a quote.

Sift is a strong Kount alternative for digital businesses where account fraud and payment fraud are both significant concerns and where behavioral analysis across the customer journey provides a meaningful signal.

For payment companies with regulatory AML requirements or merchant fraud exposure, the account-focused orientation is a limitation.

FraudNet is a fraud analytics and orchestration platform targeting large financial institutions and enterprises that need to combine multiple fraud signals, data sources, and ML models in a configurable environment.

Their Federated Machine Learning approach allows organizations to draw on a broad consortium of transaction data while maintaining data privacy, and their platform supports real-time orchestration across fraud signals from multiple internal and external sources.

FraudNet positions itself as a fraud intelligence hub rather than a single-model fraud detector.

FraudNet's orchestration approach gives large financial institutions the ability to incorporate existing fraud tools and models alongside new signals, which is valuable for organizations with complex internal architectures they cannot easily replace.

Fraud.net offers custom pricing based on organizational requirements, transaction volumes, and modules required. No standard public tiers are listed. Contact their sales team for a customized plan.

FraudNet is amongst the best Kount alternatives for large financial institutions that need a configurable fraud orchestration layer and have the technical resources to operate it.

For payment companies that need a fast-deploying, low-configuration fraud solution, the setup complexity and enterprise orientation create barriers that other tools on this list avoid.

Feedzai is one of the most established names that comes up when comparing the best Kount competitors for enterprise-grade financial services. Their RiskOps platform covers omnichannel fraud detection across card payments, account fraud, AML, and financial crime operations, processing a claimed $8 trillion in annual payment volume.

Feedzai is deployed at major banks in the US and Europe and has positioned itself as an AI powerhouse in financial crime detection, backed by analyst recognition from Gartner and Forrester. Their whitebox explainability layer is particularly relevant for regulated institutions that need to justify automated fraud decisions to regulators.

For large financial institutions seeking Kount alternatives, Feedzai offers proven scale and regulatory credibility that few platforms can match. The trade-off is a product and pricing model built for enterprise complexity, not mid-market accessibility.

Feedzai's scale credentials, analyst recognition, and regulatory explainability give it strong credibility for tier-one institutions that need enterprise-grade omnichannel fraud and AML coverage.

The RiskOps framing aligns well with institutions trying to consolidate fragmented fraud and compliance tool stacks – positioning them amongst the best Kount alternatives in the market for this segment.

Feedzai operates on custom enterprise pricing. No publicly available tiers exist. Multi-year contracts with implementation and consulting fees are standard. Contact Feedzai's sales team for pricing.

Feedzai is amongst the best Kount alternatives for tier-one and tier-two financial institutions that need proven enterprise-scale omnichannel fraud and AML coverage with regulatory explainability.

The integration timeline, contract structure, and pricing model make it inaccessible for mid-market payment companies and fintechs, which is where tools like Fraudio and SEON are better fits.

Sardine is a fraud detection platform founded by former Coinbase and Revolut executives, built originally for the neobank and crypto use case before expanding to broader financial services.

Their differentiation is in device intelligence and behavioral biometrics: Sardine profiles 2.2 billion devices and uses sub-50ms decision speed to evaluate fraud risk at the moment of account opening, transaction processing, or fund movement.

Sardine covers account fraud, payment fraud, and crypto-specific fraud vectors, and has expanded to include ACH, wire, and crypto transaction monitoring.

For teams at fintechs and digital banks exploring best Kount alternatives due to limited device intelligence, Sardine offers deeper device-level signals and faster decisions than most options in this list.

Sardine's combination of speed, device intelligence depth, and neobank-native origin makes it one of the best Kount alternatives for digital financial services companies that find Kount's device signals insufficient.

The 2.2 billion device network in particular provides a meaningful signal for detecting repeat fraudsters across multiple organizations.

Sardine uses custom pricing based on transaction volume and deployment scope. Contact their sales team for a direct quote.

Sardine is amongst the best Kount alternatives for fintechs, neobanks, and crypto platforms where device intelligence and behavioral biometrics are the primary fraud detection requirement.

For traditional acquirers and payment facilitators needing merchant fraud detection or full AML transaction monitoring, the device-first orientation is a product coverage limitation.

Featurespace is an enterprise AI company best known for its ARIC Risk Hub, which uses Adaptive Behavioral Analytics to detect fraud at tier-one financial institutions including HSBC, NatWest, and Worldpay.

Founded in Cambridge and commercialized out of Cambridge University research, Featurespace's technology models individual user behavior over time and detects anomalies that deviate from each person's established behavioral pattern.

This approach is particularly effective at catching account takeover and complex fraud patterns that rule-based systems miss.

Its pricing and complexity keep it out of reach for most mid-market buyers, but for tier-one banks running large-scale fraud programs it is one of the stronger options in this list.

Featurespace's individual behavioral modeling approach is more sophisticated than Kount's identity trust network for financial institutions where detecting account-level anomalies is the primary concern.

For organizations where analyst recognition and enterprise credibility are procurement requirements, Featurespace's 70+ major bank deployment base is hard to match.

Featurespace uses custom enterprise pricing based on transaction volume, accounts monitored, modules deployed, and level of customization.

Monthly, annual, or bespoke billing cycles are also available. Contact Featurespace's sales team for pricing.

Featurespace is one of the best Kount competitors for tier-one and tier-two banks that need adaptive behavioral analytics at proven enterprise scale and where analyst recognition is a procurement factor.

The pricing, implementation complexity, and enterprise-only positioning make it unsuitable for most emerging fintechs, payment facilitators, and mid-market payment companies.

A genuine Kount alternative needs to deliver real-time fraud scores at the point of authorization without a months-long ramp-up period.

The most common weakness of legacy fraud platforms, including siloed AI competitors to Kount, is that detection accuracy is low for the first 6 to 12 months while the model trains on each customer's own data.

Any tool claiming to be among the best fraud detection solutions should be able to demonstrate detection capability from the first day of operation.

Kount's primary strength is transaction-level card fraud. Organizations that also need merchant fraud detection, AML transaction monitoring, or P2P transfer monitoring typically find that Kount requires additional vendor relationships to fill those gaps.

The best Kount alternatives often cover multiple fraud vectors in a single integration, reducing operational overhead and data fragmentation.

A 5 to 14-month integration timeline is a structural problem for any organization experiencing active fraud spikes or scaling rapidly.

The best Kount alternatives on the market usually offer API-first integration that can go live within days to weeks.

This is not a minor convenience; for a payment facilitator experiencing merchant fraud while its current tool is under contract, the integration timeline determines how much financial exposure accumulates before the new tool takes effect.

Enterprise contracts with fixed annual fees, setup costs, and consulting charges create pricing structures that penalize growth.

A payment company processing 50 million transactions per month should not face the same total cost of ownership as one processing 5 billion.

The best Kount alternatives offer usage-based pricing where the cost per transaction decreases as volume grows, aligning the vendor's economics with the customer's growth trajectory.

For payment companies in the EU, Middle East, South Asia, and Southeast Asia, data residency compliance is a hard requirement, not a preference.

Any alternative that cannot deploy in the territory where transaction data is generated is not a viable alternative for those organizations. Verify specifically, not just in principle.

Before evaluating the best Kount alternatives, clarify which fraud vectors are your most significant exposure: card fraud at the transaction level, fraudulent merchant activity in your acquiring portfolio, money laundering requiring AML transaction monitoring, APP fraud in your P2P transfer flows, or identity fraud at onboarding.

Different tools on this list address different vectors; choosing based on a feature comparison without anchoring to your primary risk exposure wastes evaluation time.

If your engineering team is at capacity or your fraud exposure is growing faster than a multi-month integration allows, rule out any tool that cannot deploy within your required timeline.

Ask specifically: what does integration look like for a company with our architecture, and what has your median time-to-live been for customers of similar complexity?

Transaction-fee models (Stripe Radar), per-seat or per-module enterprise contracts (Feedzai, Featurespace), and usage-based per-transaction pricing (Fraudio, SEON) all behave differently as your transaction volume grows.

Model the cost at your current volume and at 3x your current volume.

A tool that looks affordable today may be your most expensive operational cost in two years if pricing is not volume-aligned.

Several tools on this list claim to use shared or federated data networks for fraud detection. The quality of these network effects varies significantly.

Ask specifically:

Fraudio's patented centralized dataset is a specific architectural claim; verify similar specificity from any competitor making network effect claims.

If your transactions are processed in regulated territories (EU, KSA, UAE, India, Indonesia), confirm not just that the vendor is GDPR-compliant but that they have a physical deployment in the data residency territory you operate in.

This is not a checkbox exercise; ask for proof of existing customer deployments in your specific territory.

Fraudio is the only fraud and AML platform in this list with a patented centralized dataset that delivers genuine network effects across all connected customers from day one. We cover four fraud vectors in a single integration: card fraud, merchant fraud, AML, and P2P transfer monitoring.

We integrate in 3 to 14 days, not months – plus, we charge per transaction with no setup fees, so your costs align with your transaction volume, not with a vendor's commercial structure.

Fraudio is built for payment companies: issuers, acquirers, payment facilitators, fintechs, and digital banks that process real payment volume and need fraud detection that matches their pace of growth and the regulatory environment they operate in.

Post signing up for a demo, you’ll see why Viva Wallet achieved 8x ROI, a 600% increase in fraud team efficiency, and fraud caught 3 weeks earlier than their previous solution.

The same result is available with your historical data before you commit to a full deployment.

If your fraud challenge lives at the transaction layer and using Kount isn’t yielding the desired results, book a demo with Fraudio or request a Proof of Results test using your historical data.

Kount is a fraud prevention platform primarily used by eCommerce merchants and payment companies to reduce chargebacks, detect account takeover, and manage payment authorization fraud. It combines device signals, behavioral data, and identity information through its Identity Trust Network, and it was acquired by Equifax in 2021. Teams most commonly use it to protect against card-not-present fraud and account abuse in online transactions.

Fraudio tops the list for the best Kount alternatives in 2026. We’re the best fit for payment companies who require real-time fraud, AML and merchant fraud detection capabilities in a single platform. You can also explore the likes of SEON, Feedzai, Sardine and Stripe Radar based on your business context, requirements and use cases. Ultimately, the right choice depends on your specific fraud vectors, integration constraints, and team size.

The most important features to look for in a Kount alternative are: real-time transaction scoring with immediate detection capability from day one rather than months-long ramp-up, coverage across your primary fraud vectors (card fraud, merchant fraud, AML, P2P), integration timeline in days rather than months, usage-based pricing that scales with transaction volume, and verified data residency compliance in the territories where you operate.

You can choose the best Kount alternative by first identifying your primary fraud vectors (card fraud, merchant fraud, AML, P2P transfers, identity fraud), then filtering by integration timeline, pricing model at your projected 3x volume, and verified data residency capability. Run a Proof of Results test or trial using historical data before committing. We at Fraudio also offer a no-commitment PoR test using your historical data to demonstrate detection quality before any contract is signed.

Switching from Kount to an alternative depends on the tool you choose. Fraudio integrates via API in 3 to 14 days, and a Proof of Results test can run in parallel with your existing Kount deployment using historical data before you switch. On the other hand, SEON deploys in approximately 14 days. Enterprise alternatives like Feedzai and Featurespace carry integration timelines of 5 to 14 months. Running a parallel test during your remaining Kount contract period is the standard approach to reduce the risk of any gap in coverage.

Fraudio offers a much wider range of fraud coverage than Kount, which mostly focuses on transaction-level card fraud for merchants. We also handle merchant-initiated fraud (MIF), P2P transfer monitoring, and full AML with case management. For payment companies, this means you get all four fraud vectors covered in a single platform without needing multiple vendors.

Fraudio's Proof of Results (PoR) is a low-commitment way to see detection quality before full deployment. You provide historical transaction data with no live integration needed, and we compare its detection against your current tool's performance on the same transactions. Unlike a 30-day trial requiring engineering time, PoR runs in parallel without touching production. For organizations mid-contract with Kount, you can build a switching business case before renewal. Next step is a Proof of Concept with live integration and an exit clause.

How about trying our solution and experiencing the next generation for yourself?