March 18, 2026

Last Updated: March 11, 2026

Payment fraud detection software consists of specialized platforms designed to monitor, identify, and prevent fraudulent payment transactions in real time.

These tools use a combination of technologies - including machine learning, artificial intelligence (AI), behavioral analytics, and predefined rules - to analyze transaction data and flag suspicious activities. The goal is to stop financial criminals before they can cause damage, protecting both businesses and their customers.

The industry has evolved significantly from simple, rule-based systems to sophisticated, AI-driven payment fraud detection platforms.

Modern solutions analyze hundreds of data points for each transaction, such as device information, location, purchase history, and payment method. This allows them to detect complex fraud patterns that would be impossible for human teams to catch.

As e-commerce and digital payments continue to grow, these top fraud detection solutions for payments have become essential for any business processing transactions online.

Every business that accepts payments is a target for fraud.

The consequences go far beyond a single lost transaction. You face financial losses from chargebacks, penalties from card networks, and damage to your brand's reputation.

According to recent reports, businesses lose over 5% of their annual revenue to fraud each year. An effective payment fraud detection software acts as your first line of defense, mitigating these risks and safeguarding your bottom line.

The core problem these platforms solve is the inability to scale fraud prevention manually. Fraudsters use automated bots and sophisticated schemes to attack businesses 24/7. A manual review process is too slow, expensive, and prone to error.

By automating the detection process, you can approve more legitimate transactions faster, reduce false declines that frustrate good customers, and free up your team to focus on strategic initiatives. This transformation from reactive to proactive fraud management is critical for sustainable growth.

Various organizations across the payment ecosystem require robust fraud detection capabilities.

The specific needs may differ, but the underlying goal remains the same: to secure transactions and protect assets.

PSPs and acquirers sit at the center of the payment flow, making them a prime target.

They need a solution that can monitor transactions for millions of merchants simultaneously, identify cross-merchant fraud patterns, and offer fraud protection as a value-added service to their portfolio.

Card issuers and the processors that serve them need to protect cardholders from unauthorized use across all transaction types - card-present, card-not-present, and instant payments.

They require real-time scoring at the point of authorization combined with robust AML capabilities to meet regulatory obligations.

Payment facilitators manage sub-merchants, inheriting the risk associated with their transaction activity.

They need a multi-tenant solution that allows them to onboard merchants quickly while maintaining complete oversight and control over fraud risk.

Approximately 3% of new digitally boarded SMEs turn out to be fraudsters, making proactive merchant monitoring essential.

Digital-first financial institutions face unique exposure to Authorized Push Payment (APP) fraud and money mule networks.

They need a platform that can monitor peer-to-peer transfers and account-to-account payments in real time, detecting coordinated fraud campaigns before funds are dispersed.

Companies operating cross-border remittance or instant payment networks must monitor high volumes of transfers across multiple jurisdictions, often with strict data residency requirements.

They need a solution that can deploy locally, adapt to regional regulatory frameworks, and flag suspicious activity without adding friction to legitimate transfers.

Companies that serve payment businesses - such as issuing processors, acquiring processors, payment gateways, and orchestrators - need a flexible, white-label fraud solution.

This allows them to resell fraud detection services, create a new revenue stream, and provide more value to their clients without building detection capabilities from scratch.

Here is an in-depth payment fraud detection tools comparison to help you find the right solution for your business.

Fraudio is an AI-powered financial crime prevention platform built for the entire payment ecosystem.

It solves the core problem of siloed fraud data by creating a centralized network that connects issuing and acquiring data streams. This unique approach gives Fraudio's AI an unparalleled view of transaction behavior, enabling it to detect sophisticated fraud that other systems miss.

The platform is designed for payment service providers, acquirers, and large enterprises that need a flexible, powerful, and easy-to-use solution to combat payment fraud.

Fraudio’s primary advantage is its powerful network effect. By being a third-party focused solely on financial crime, we can legally centralize data from both the issuing and acquiring sides of a transaction–something a processor cannot do. This gives our AI a complete picture, identifying fraud rings and patterns that are invisible to siloed systems.

Our platform’s flexibility is another key differentiator; it’s designed for ease of use, allowing any data point to be accessed in just a few clicks.

Finally, our multi-tenancy environment enables partners to resell our capabilities independently, creating new revenue streams with full control.

Fraudio offers custom pricing based on transaction volume and the specific needs of the client. This ensures a value-based model where the cost aligns with the protection provided.

Fraudio is the best payment fraud detection software for any organization that is serious about stopping financial crime at its source.

Its unique ability to centralize and analyze data from the entire payment lifecycle provides a decisive advantage over competitors.

The platform's combination of power, flexibility, and speed makes it the top choice for PSPs, acquirers, large merchants, and partners who need a scalable and future-proof solution.

Sift is a well-known name in the fraud detection space, offering a "Digital Trust & Safety Suite."

Its platform leverages real-time machine learning to help businesses prevent payment fraud, account takeovers, and content abuse. Sift is particularly popular among digital e-commerce businesses and marketplaces that need to make instant trust decisions at scale.

Sift is one of the strongest choices for businesses focused on user-generated content and account security, in addition to payment fraud.

Its console is generally considered user-friendly, and it provides a comprehensive suite of tools that covers more than just payments.

This makes it a smart option for trust and safety teams dealing with multiple forms of online abuse.

Sift uses a quote-based pricing model that depends on transaction volume, monthly active users, and the specific products used.

Sift is a powerful and reliable platform, especially for customer-facing digital businesses that need an all-in-one solution for trust and safety.

However, its broader focus means it may not have the depth in payment-specific data analysis (like combining issuing and acquiring data) that a specialized provider like Fraudio offers.

It's a great tool, but might not be the top choice for organizations whose primary challenge is complex payment fraud.

Feedzai positions itself as a comprehensive RiskOps platform, designed primarily for large financial institutions and banks.

It uses advanced AI and machine learning to manage fraud and financial crime across the entire customer lifecycle, from onboarding to payments and AML compliance.

Feedzai is known for its robust case management and ability to handle massive transaction volumes.

Feedzai's strength lies in its enterprise-grade capabilities and its focus on the regulated financial services industry.

Its ability to provide a unified solution for both fraud and anti-money laundering (AML) is a significant advantage for banks and large fintechs that need to manage both.

It is a smart choice for organizations requiring deep case management and reporting features for compliance purposes.

Feedzai’s pricing is quote-based and tailored to the needs of large enterprise clients.

For large global banks and financial institutions needing an all-encompassing platform for financial crime, Feedzai is a top contender. It is built for scale and regulatory complexity.

However, its high cost, complexity, and long implementation times make it unsuitable for most merchants, PSPs, and businesses that need an agile and fast-to-implement solution focused purely on payment fraud.

Forter is a fully automated fraud prevention platform focused on e-commerce.

Its primary value proposition is its ability to provide real-time approve/decline decisions with a chargeback guarantee.

This hands-off approach is designed to maximize approval rates and shift the liability for fraudulent chargebacks from the merchant to Forter.

Forter's chargeback guarantee model makes it a compelling choice for enterprise retailers who want predictable costs and minimal operational overhead.

By taking on the liability for fraud, it allows businesses to focus entirely on growth. This makes it one of the strongest options for merchants prioritizing revenue optimization above all else.

Forter’s pricing is quote-based, typically structured as a percentage of the transaction volume it approves.

Forter is a great choice for large e-commerce merchants who are willing to pay a premium to outsource their fraud management and maximize approvals.

However, the lack of control and transparency makes it a poor fit for businesses that want to manage their own risk strategy, PSPs that need to offer configurable solutions to their merchants, or companies that require deep insights into fraud patterns.

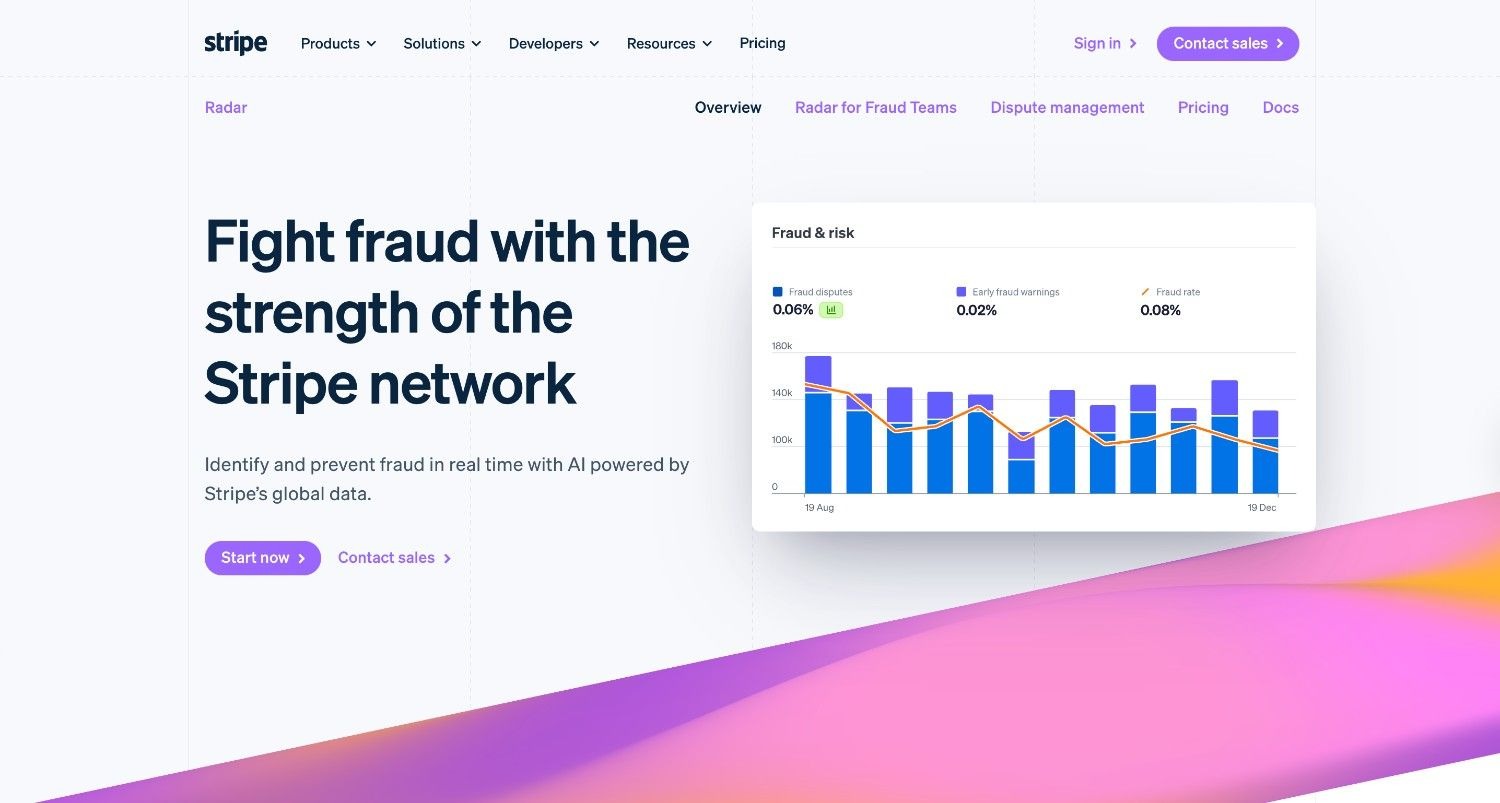

Stripe Radar is a fraud detection tool built directly into the Stripe payments platform.

It uses machine learning that trains on data from millions of businesses on the Stripe network to help identify and block fraudulent payments.

There are two versions: Radar, which is included with Stripe's standard processing fees, and Radar for Fraud Teams, which adds more powerful, customizable features for a fee.

Stripe Radar’s biggest advantage is its convenience.

For the millions of businesses that use Stripe, it is the most straightforward and cost-effective way to get started with fraud prevention. The fact that a powerful machine learning tool is included by default is a massive benefit for small businesses that couldn't otherwise afford a dedicated fraud solution.

Stripe Radar is included with Stripe's standard transaction fees (2.9% + 30¢). Radar for Fraud Teams costs an additional 2¢ per screened transaction.

If your business runs entirely on Stripe, Radar is a smart choice. It provides excellent baseline protection for a very low cost.

However, it is not a viable solution for businesses that use multiple payment processors, operate as a PSP, or require sophisticated, cross-acquirer fraud analysis.

It’s a great feature of a payment platform, but not a standalone, top-tier payment fraud detection platform.

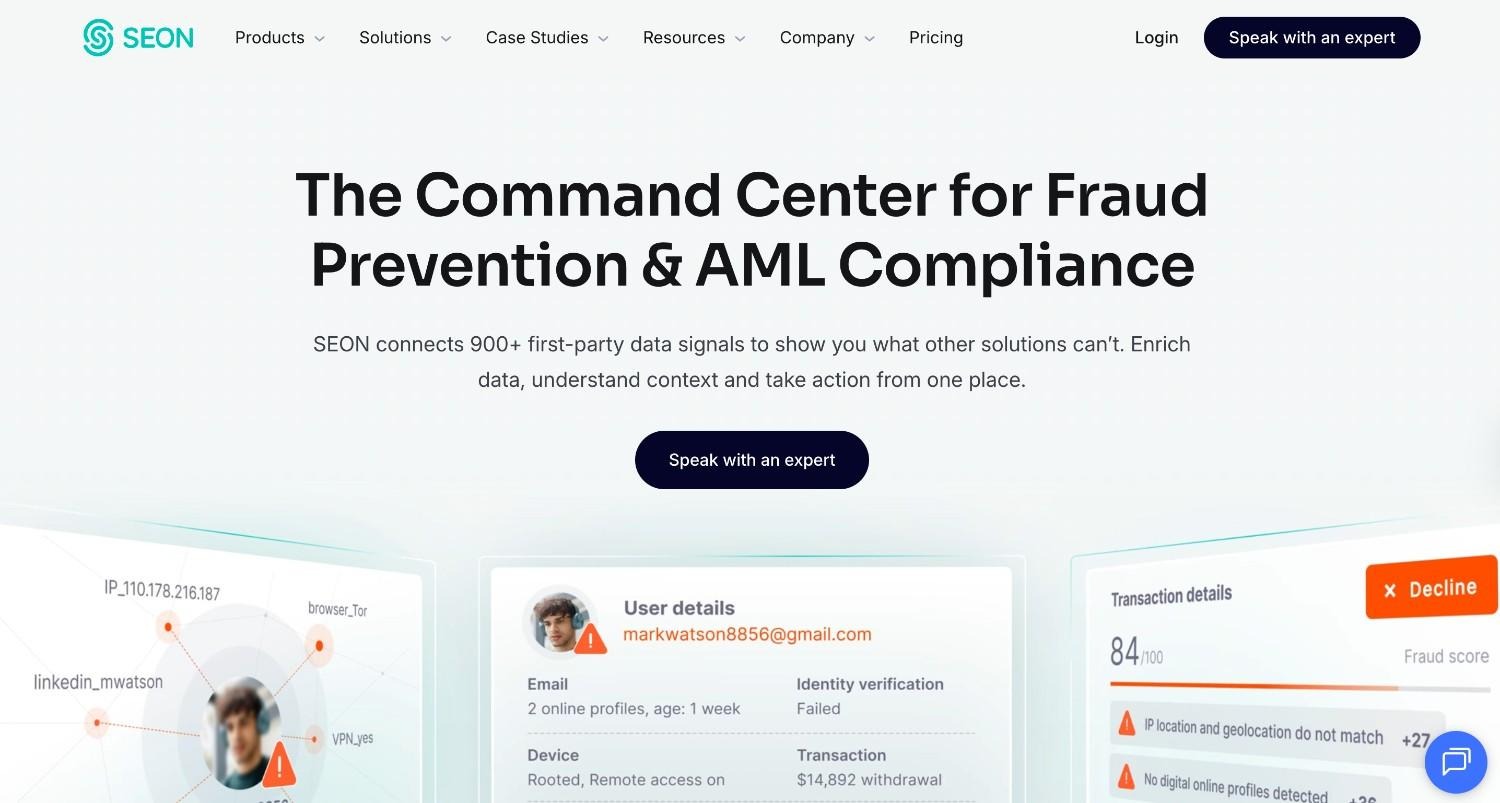

SEON is a fraud prevention platform that focuses on enriching data to build a complete profile of a user.

It stands out by using digital footprinting–analyzing a user's email address, phone number, and IP address to check for their presence on over 50 social and digital platforms.

This helps businesses verify if a user is legitimate or a fraudster using a fake identity.

SEON's data enrichment capabilities are a strong differentiator.

While other platforms focus on transaction patterns, SEON excels at determining who is behind the transaction.

This makes it a very powerful tool for manual reviews and for businesses that struggle with synthetic identity fraud.

SEON offers a free plan and paid plans starting from $599/month. They also offer a flexible, pay-as-you-go model for API calls.

SEON is a fantastic tool for businesses that want to augment their fraud detection with deep user intelligence. It is particularly effective for industries where identity verification is key.

However, it may not be the best primary solution for organizations processing massive payment volumes that need a platform focused on the network-level analysis of transaction flows, like a payment acquirer.

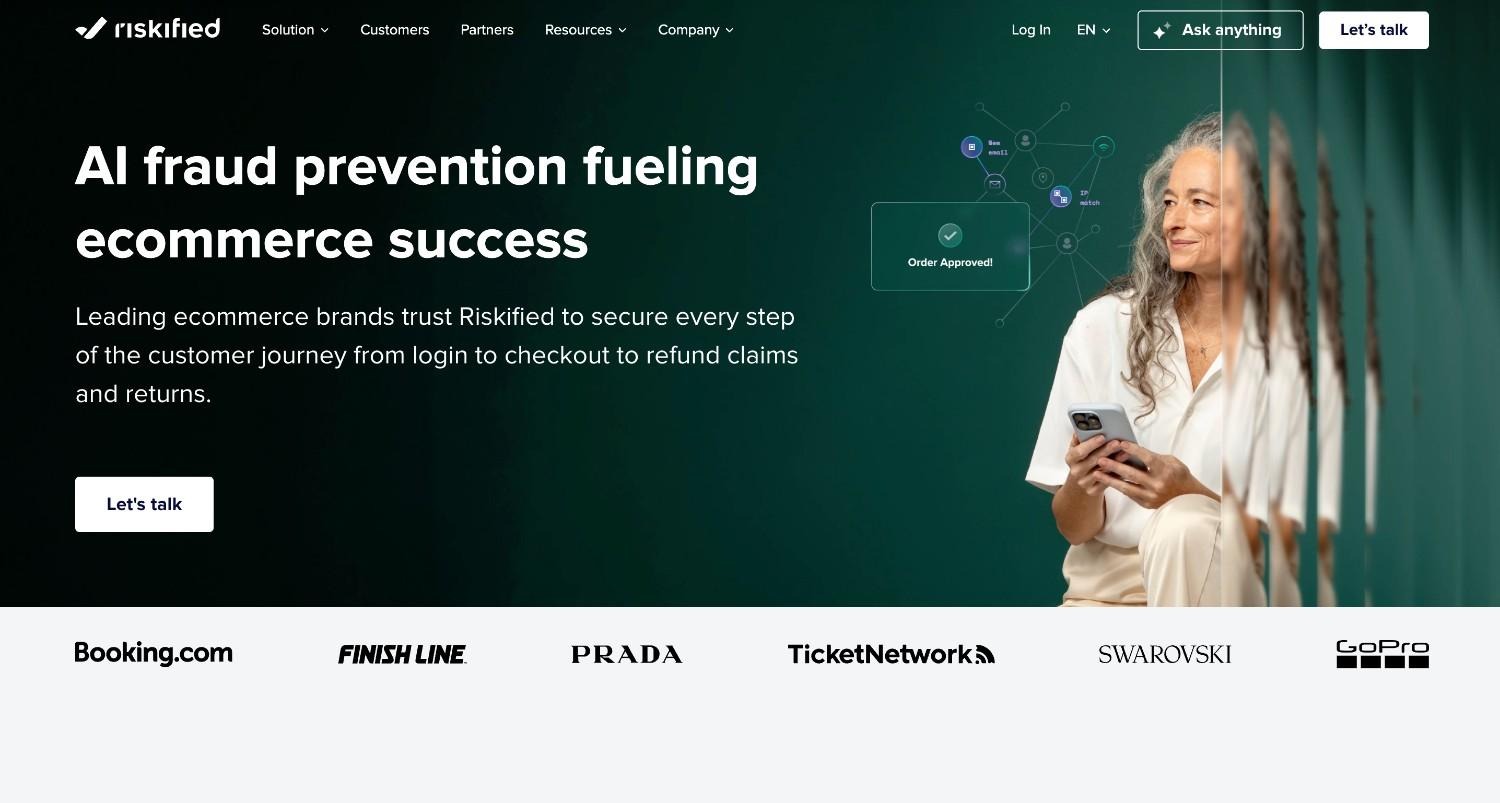

Similar to Forter, Riskified is a fraud management platform for e-commerce that offers a chargeback guarantee. It uses machine learning to make approve/decline decisions and aims to help merchants safely approve more orders and increase revenue.

The platform also provides insights into customer behavior and can help optimize checkout flows for regulations like PSD2.

Riskified’s focus on revenue maximization and its chargeback guarantee model make it a strong contender in the enterprise e-commerce space.

Its expertise in navigating complex regulatory environments like Europe’s PSD2 is a key advantage for global merchants.

Riskified provides custom, quote-based pricing, usually as a fee per approved transaction.

Riskified is a great choice for large online retailers who are focused on growth and want a hands-off fraud solution. Its guarantee model is appealing for financial predictability.

However, like Forter, it's not the right fit for PSPs, acquirers, or any business that needs control, transparency, and the ability to analyze fraud across different payment channels and processors.

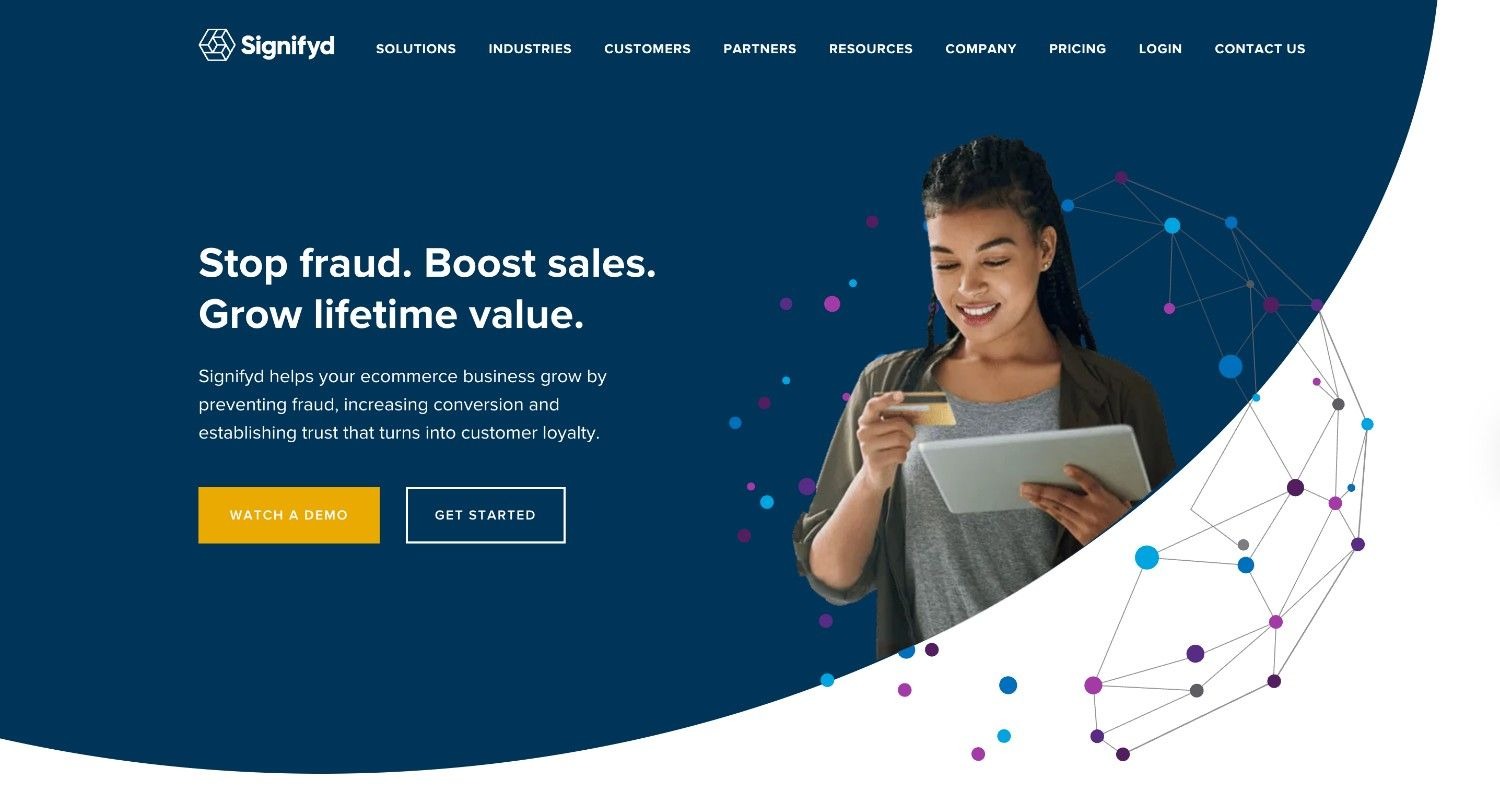

Signifyd provides a "Commerce Protection Platform" aimed at e-commerce merchants. It combines payment fraud detection with solutions for item-not-received (INR) claims and policy abuse (like promo code or returns abuse).

Like Forter and Riskified, its core offering is a financial guarantee against fraudulent chargebacks.

Signifyd's decision to tackle non-fraud chargebacks and policy abuse sets it apart.

Many merchants lose significant revenue to claims of items not being received or to customers exploiting liberal return policies. By addressing these issues, Signifyd offers a more holistic protection solution for e-commerce P&Ls.

Signifyd offers custom pricing based on the merchant's sales volume and risk profile.

For e-commerce merchants who are losing revenue to a wide range of chargebacks and abuse, Signifyd is a very compelling option. Its broader focus on "commerce protection" can deliver a strong ROI.

However, its purpose is narrow; it is not a flexible payment fraud detection platform for payment processors or businesses with complex, multi-acquirer payment flows.

LexisNexis Risk Solutions provides a suite of tools for fraud detection, identity verification, and risk management.

Its offering is built around the ThreatMetrix product, which leverages a massive global network of digital identity intelligence. It helps businesses distinguish between trusted customers and potential fraudsters in real time based on their device, location, and behavior.

The sheer scale of the LexisNexis Digital Identity Network is its biggest asset. This vast repository of data on devices, identities, and behaviors gives it powerful insights into both legitimate and fraudulent activity.

This makes it a smart choice for global corporations that need to verify users from all corners of the world.

LexisNexis provides custom, enterprise-level pricing based on usage and the specific solutions deployed.

LexisNexis Risk Solutions is an enterprise-grade powerhouse for digital identity verification and fraud prevention. It is a smart choice for large, multinational corporations that need a robust, data-rich solution.

However, it can be overly complex and expensive for mid-market businesses or PSPs looking for a more agile and payment-flow-centric fraud platform.

NICE Actimize is a leader in the enterprise financial crime software market.

Its platform offers end-to-end solutions covering fraud, anti-money laundering (AML), and trading surveillance, primarily for large financial institutions.

Its strength lies in its highly configurable case management, workflow automation, and robust compliance features.

NICE Actimize is a market leader for a reason: it offers one of the most comprehensive and configurable platforms for enterprise financial crime management.

Its deep roots in banking and compliance make it a trusted partner for the world's largest financial institutions.

NICE Actimize offers premium, enterprise-level pricing available only via a custom quote.

For a top-tier global bank that needs a single, comprehensive system to manage all facets of financial crime and compliance, NICE Actimize is one of the best choices available.

However, it is the antithesis of a nimble, easy-to-integrate solution.

It is not suitable for any organization outside of the large enterprise financial services sector.

Selecting the right payment fraud detection software is a critical decision.

Here are the key factors to consider to ensure you choose the best platform for your needs.

The effectiveness of any AI-based fraud detection system depends on the quality and breadth of its data. Ask potential vendors about their data sources. Do they only see data from their direct customers, or do they have a wider network?

A platform that centralizes data from across the payment ecosystem - including both issuing and acquiring sides - will always have a significant advantage in detecting complex fraud patterns.

Siloed AI models that learn only from a single customer's data require months of ramp-up and will always have blind spots.

Your business is unique, and your fraud strategy should be too. A rigid, "black box" solution may work for some, but most businesses need control.

Look for a platform with a flexible rule engine that allows your team to create and adjust rules easily, without requiring engineering resources for every change.

The ability to consume any type of payment data and adapt to your existing systems - whether via real-time API, webhook, or batch processing - is essential for long-term agility.

In the fast-moving world of fraud, you can't afford to wait months for a solution to go live.

Inquire about the typical integration timeline. Does the vendor have pre-built connectors with your existing partners? Can you access rule libraries from day one?

Does the platform's AI protect you from the very first transaction processed, or does it require a long training period? A fast go-to-market means you start protecting your revenue sooner and can demonstrate ROI to leadership quickly.

Choose a solution that can grow with your business.

For PSPs, acquirers, or resellers, a multi-tenant architecture is non-negotiable - this allows you to manage different clients or sub-merchants from a single platform, with separate controls and reporting for each.

Ensure the platform is built on a modern, cloud-native infrastructure that can handle your peak transaction volumes without issue, and that it can support all the payment types you process today and plan to offer tomorrow.

If you operate in - or plan to expand into - regulated markets such as Saudi Arabia, the UAE, India, or Indonesia, data residency requirements are a hard constraint.

Many platforms cannot deploy locally in these territories, forcing workarounds that may put you out of compliance.

Verify that your vendor has proven, live deployments in the regions you need, not just theoretical capability.

Don't just look at the sticker price. Consider the full picture: setup fees, implementation costs, maintenance, and the internal resources required to manage the platform day-to-day.

A transparent, usage-based pricing model with no hidden fees can deliver a significantly lower total cost of ownership than a cheaper but more labor-intensive tool.

Also factor in the cost of not having an effective solution - chargebacks, regulatory fines, lost customers, and reputational damage add up fast.

This table provides a high-level top fraud detection software for payments features and comparison, giving you a quick overview of the leading options.

Choosing the right payment fraud detection platform is one of the most important decisions you can make to protect your business.

While many solutions offer effective features, Fraudio stands apart. Our unique ability to centralize data from the entire payment ecosystem gives our AI an unbeatable advantage, allowing us to spot fraud that others simply cannot see.

Don't settle for a solution that only sees half the picture. Empower your business with the most flexible, powerful, and easy-to-use fraud prevention platform on the market. Protect your revenue, delight your customers, and stay ahead of the criminals.

Get started with our free trial right now.

The best payment fraud detection software in 2026 is Fraudio, due to its unique centralized data network that combines issuing and acquiring data for superior AI accuracy. Its platform offers unparalleled flexibility and a fast go-to-market, making it the top choice for payment providers, acquirers, and large enterprises. While other tools like Sift and Feedzai are strong, they lack Fraudio's holistic data advantage.

When choosing the right payment fraud detection software, you should consider five key factors. Evaluate the breadth and depth of the provider's data network, as more data leads to better AI. Assess the platform's flexibility for creating custom rules and adapting to your business needs. Check the speed of implementation, the platform's scalability and architecture, and the total cost of ownership beyond just the subscription price.

Fraudio differs from alternatives by legally centralizing payment data from both the issuing (bank) and acquiring (merchant) sides into one unified network. This provides a complete picture of the transaction lifecycle that competitors who only see one side cannot match, leading to higher detection rates. Additionally, Fraudio's platform is built for extreme flexibility, with an LLM-powered rule engine and a multi-tenant architecture designed for partners and resellers, setting it apart from more rigid or merchant-only focused solutions.

To get started with Fraudio, you can book a free trial through our website. The integration process is designed to be fast, and our team will guide you through connecting your data, setting up the platform, and configuring initial rules. Thanks to our streamlined process and pre-built connectors, most customers can be live and seeing value in as little as two weeks.

Switching to Fraudio is a straightforward process designed to minimize disruption. Our dedicated onboarding team works with you to map your existing data flows and rules to our platform. We can run in a "shadow mode" to compare our results with your current system before you fully switch over, ensuring a seamless transition. The process is typically completed within a few weeks.

While Fraudio is powerful enough for the largest global payment providers, it is not exclusively for them. Our solution is ideal for any business that processes a significant volume of transactions and needs a highly accurate and flexible fraud solution, including mid-sized PSPs, payment facilitators, and rapidly growing e-commerce merchants. The key is the need for sophisticated protection, not just company size.

Fraud detection is the process of identifying suspicious activities, while fraud prevention is the action taken to stop that activity from causing harm. A good payment fraud detection software does both; it uses its detection engine to identify a potentially fraudulent transaction in real time and then takes preventative action, such as blocking the payment or flagging it for review. Effective platforms automate this entire workflow.

How about trying our solution and experiencing the next generation for yourself?