April 21, 2026

Last Updated: April 21, 2026

Multi-tenancy is a software architecture where a single instance of an application serves multiple customers, called tenants. Each tenant's data, configuration, and access are isolated from every other tenant, but the underlying code, infrastructure, and (often) data schema are shared.

Think of it like an apartment building.

The building is one structure with shared plumbing, electricity, and foundations. Each apartment has its own locked door, furnishings, and residents. The landlord manages the building as a whole, while each resident controls what happens inside their unit.

In fraud prevention and payment infrastructure, multi-tenancy goes a step further. A parent company (the master tenant) can not only operate its own environment but also create and manage subtenants underneath it. Each subtenant has its own users, rules, APIs, and reports, all running on the same shared platform.

The pattern becomes powerful when paired with a centralized data schema. Instead of each tenant running a separate database and a separate AI model, all customer data maps into one unified schema. Tenants remain logically separated, but the underlying intelligence sees the whole picture.

Payment infrastructure companies sit on top of huge portfolios.

A single issuer processor may serve 50 banks. A single acquirer processor may serve dozens of acquirers, who in turn serve hundreds of payment facilitators (PayFacs) and thousands of merchants.

Running a separate fraud and AML stack for each of those entities is not workable. Integration alone would take years, and operating 50 disconnected instances creates data silos that weaken detection. Multi-tenancy solves this by giving the top-level customer a single environment they can carve up.

The architecture rests on three building blocks.

1. A centralized data schema: Every transaction, merchant record, account, and signal from every tenant flows into one shared data model. This is what allows the same AI engine to learn from billions of transactions across the entire network.

2. A tenant hierarchy: The master tenant sits at the top. Subtenants sit below and inherit rules, policies, and controls from their parent. Sub-subtenants are supported, enabling structures like processor → acquirer → PayFac → merchant.

3. A control plane: A single orchestration layer exposes API, UI, and permission controls. The master tenant uses this layer to create new subtenants, issue API keys, configure rules, and audit activity - without opening a ticket with the vendor.

The centralized data schema is what turns multi-tenancy from a provisioning convenience into a detection advantage. When all tenants map their data to the same fields, the same models, rules, and dashboards work across the entire network.

This matters for two reasons.

First, it breaks data silos that exist inside most processors by default. A processor that handles both issuing and acquiring typically cannot connect the two sides of its own business, because of legal and architectural constraints. With multi-tenant fraud detection running on a shared schema, both sides feed the same detection layer.

Second, it makes network-effect AI possible. Models trained on billions of labeled transactions across thousands of merchants and hundreds of banks spot new fraud patterns faster than any single-customer model.

The master tenant owns the commercial relationship with the fraud platform vendor. They set the global policies, the baseline AML rules, and the fraud controls that every subtenant inherits by default.

Subtenants operate within that envelope. They can layer their own rules on top of inherited policies, run their own investigations, and manage their own users. But they cannot drop below the compliance floor the master tenant has set.

This inheritance pattern is central to multi-tenancy security. Even as the network of subtenants grows, the master tenant retains a consistent AML and fraud baseline without having to re-apply rules in every new environment.

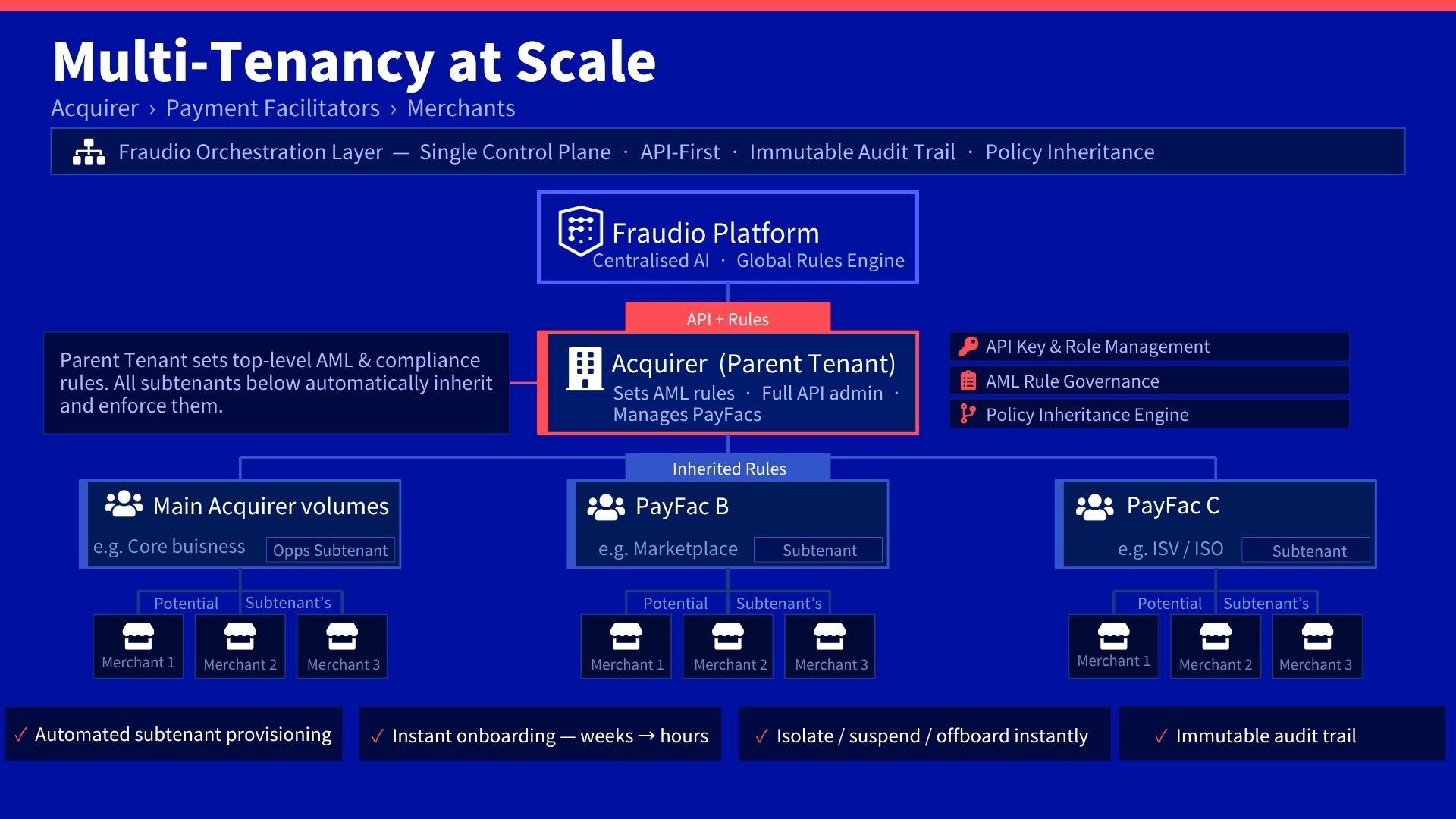

The acquiring side of the payment ecosystem stacks deep.

An acquirer processor connects POS devices, ecommerce gateways, and checkout infrastructure to the card schemes. Acquirers sit below the processor. PayFacs sit below acquirers. Merchants sit below PayFacs.

Multi-tenancy maps onto this hierarchy naturally. In a typical acquirer-led deployment:

The acquirer maintains visibility across the full tree.

If a PayFac's merchant base spikes in fraud, the acquirer sees it in their dashboard. If a new PayFac is onboarded, the acquirer creates the subtenant, provisions the API keys, and applies the starting rule set. All without a vendor ticket.

Bin sponsorship scenarios work the same way. An acquirer that bin-sponsors a super-merchant can require the super-merchant to use the fraud platform while keeping its own overlay of controls. The super-merchant gets operational autonomy. The acquirer keeps its compliance obligations covered.

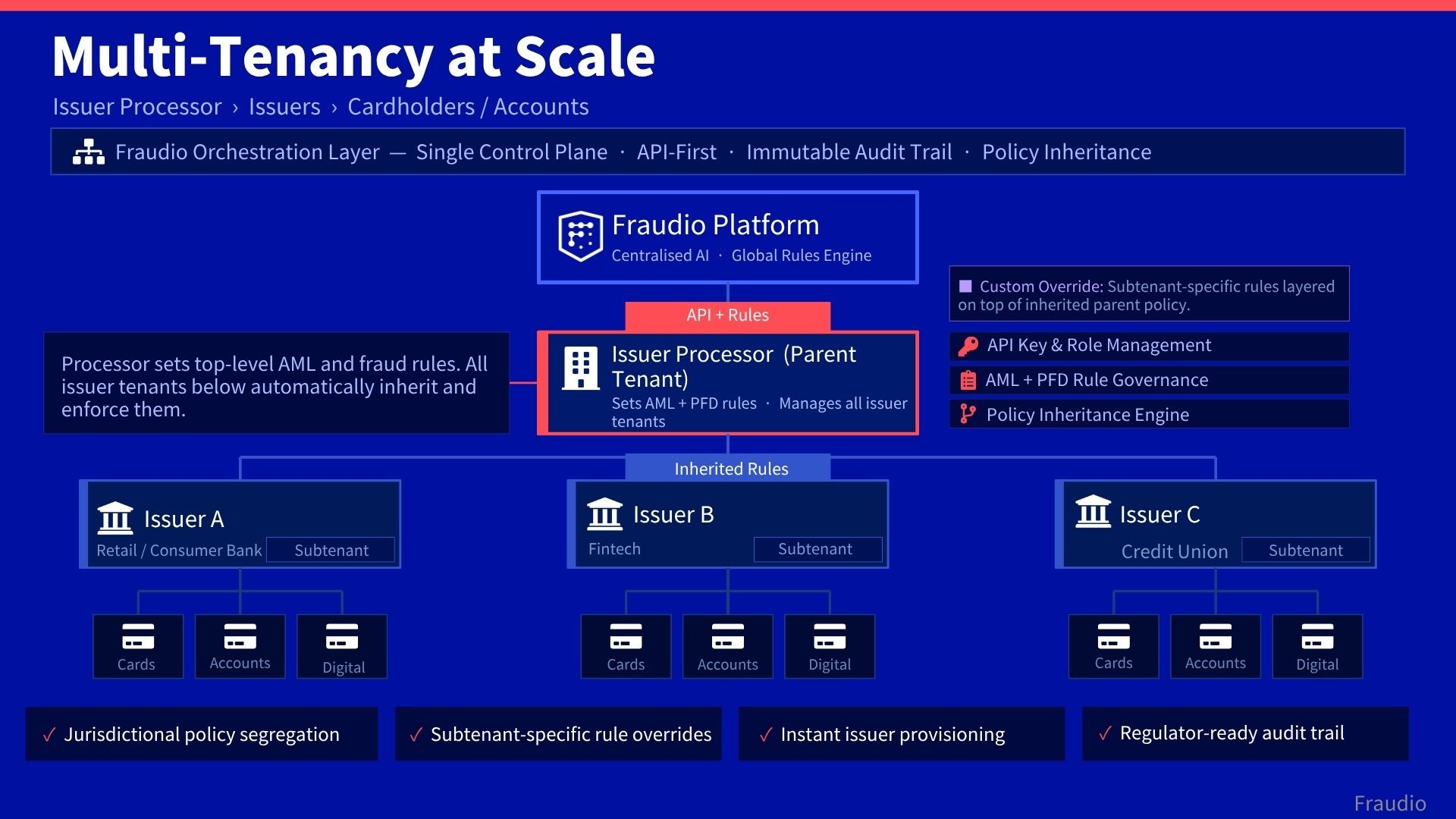

On the issuing side, the structure is different but the principle is the same.

An issuer processor provides the technology that connects banks and fintechs to Visa and Mastercard. Those banks may not hold their own direct scheme licenses; the processor does.

In an issuer-led deployment:

The processor can provision a new issuer subtenant in minutes. Rules inherit down. Each issuer gets its own API keys, its own dashboard, its own case management queue. The processor keeps a single view across all of them.

Because issuer portfolios often sit in different jurisdictions, subtenant-specific rule overrides are common. A European issuer might need to add PSD2-specific controls. A Middle East issuer may have data residency constraints. Both layer their own rules on top of the inherited parent policy; without affecting any other tenant in the tree.

The practical value of multi-tenancy comes from what the master tenant can do without vendor involvement.

A good multi-tenant implementation removes the platform vendor from the critical path of day-to-day operations:

The master tenant can create a new subtenant on demand. No ticket, no procurement cycle, no two-week integration call. The subtenant is spun up with the parent's inherited rule set, a dedicated data partition, and its own API credentials.

For a processor onboarding a new bank client, this is the difference between a three-week project and a same-day launch.

Each subtenant has its own API keys, isolated from every other subtenant. The master tenant can revoke, rotate, or suspend those keys independently.

Users sit under their subtenant. An analyst at Issuer A cannot see Issuer B's data. Roles and permissions are configured per subtenant - an admin at one subtenant has no implicit authority at another.

Not every bank or acquirer has the same risk appetite. Multi-tenancy lets the master tenant set a floor of inherited rules, then allow each subtenant to configure additional controls within that envelope.

A retail consumer bank may want tighter card-not-present (CNP) thresholds. A fintech issuer may tune for velocity on digital goods. A PayFac serving high-risk verticals will want merchant-level controls the parent acquirer does not need for its direct portfolio.

The master tenant can resell fraud prevention to its own customer base under its own brand. In a full white-label deployment, the subtenant's users never see the vendor's name - the entire interface, domain, and branding belong to the master tenant.

This supports indirect go-to-market motions. A processor can package fraud detection into its core product and monetize it across its bank portfolio. An acquirer can sell it down to PayFacs and super-merchants. One Fraudio customer already runs the product fully white-labeled across their portfolio today.

Multi-tenancy security is the main concern many compliance teams raise before they understand how modern implementations work. The worry is valid in principle: if one application serves many customers, a flaw in tenant separation could expose one tenant's data to another.

Good multi-tenant systems address this through several layers:

When these layers are designed together, multi-tenancy security can match or exceed what most single-tenant deployments deliver in practice. The shared model receives more security scrutiny, more rapid patching, and more consistent controls than dozens of bespoke environments ever would. ISO27001 certification gives the formal assurance that card schemes and regulators expect.

The choice between multi-tenancy and single-tenancy is not just operational.

It directly shapes how well fraud detection works.

Siloed single-tenant AI models learn only from the data their specific customer has seen. Every new fraud pattern has to appear, cause damage, be investigated, and be labeled before the model can pick it up. In a multi-tenant fraud platform with shared context, patterns first seen at one customer inform detection across the whole network - almost immediately.

This is why new payment platforms often hit detection ceilings with single-tenant tools. Their data volume simply is not large enough to train competitive models in a reasonable timeframe.

An issuer processor connects dozens of banks to Visa and Mastercard. Historically, each bank negotiated its own fraud tool separately. Integration times ranged from six to fourteen months. Each bank had its own vendor relationship, its own rule set, its own case management workflow.

With multi-tenancy, the processor owns the top-level contract. New bank clients are onboarded as subtenants in days, not months. The processor sets a baseline AML rule set that every bank inherits. Each bank can add its own overlays for its specific products and jurisdictions. The processor sees the whole portfolio in one view.

This turns fraud detection from a friction point in new-bank onboarding into a built-in capability the processor sells as part of its core offering.

An acquirer processor connects POS devices and ecommerce checkout to the card schemes. Their direct customers are acquirers. Acquirers' customers are PayFacs. PayFacs' customers are merchants.

With a multi-layer tenancy model, the processor can act as master tenant and make fraud prevention available to acquirers, who can make it available to PayFacs, who can make it available to their super-merchants. Each layer controls what sits beneath it. Rules inherit down. Data remains isolated across layers. The processor has visibility into the whole tree.

This is the foundation of an indirect go-to-market model. The processor sells fraud prevention once - to the acquirer - and the acquirer sells it down through its own channels, potentially under its own brand.

In bin sponsorship, an acquirer with direct scheme membership lets a super-merchant or a smaller acquirer process under its BIN. The sponsoring acquirer remains liable for fraud and compliance breaches in that sponsored portfolio.

Multi-tenancy gives the sponsoring acquirer a clean way to manage this exposure. The super-merchant operates as a subtenant. The acquirer's inherited AML and fraud rules apply by default. The super-merchant can run its own tuning on top. If something goes wrong, the acquirer has a complete audit trail and can isolate or offboard the super-merchant within minutes.

A digital wallet provider handles peer-to-peer (P2P) transfers, remittances, and account-to-account payments. APP (Authorized Push Payment) fraud and money mule networks are the dominant threats. Each new market launch means new regulators, new reporting requirements, and new fraud patterns.

A multi-tenant deployment lets the wallet operator treat each country as a subtenant with its own rules, its own case management, and its own compliance reports - while a shared AI layer still learns from cross-border patterns the whole network sees. Approximately 3% of newly onboarded digital SME merchants turn out to be fraudulent, and multi-tenant detection catches many of them weeks before chargebacks arrive.

Fraudio was built from the start as a multi-tenant fraud prevention platform with a centralized data schema. Models learn from billions of transactions across every connected customer in real time - not from each customer's isolated history. That is the patented core of the product.

Two things set it apart for payment infrastructure players.

First, network-effect AI on a shared schema: one detection engine, one rule context, applied across issuers, acquirers, PayFacs, and their merchants. Second, real master-tenant control: processors, gateways, and orchestrators provision new subtenants, rotate API keys, configure rules, and white-label the product without opening vendor tickets.

This is built for processors on both the issuing and acquiring sides, for payment gateways and orchestrators, and for acquirers who want to resell fraud prevention down to their PayFac and merchant base. Customers see integration in days rather than months, weekly platform releases, and 8x ROI in documented results with customers such as Viva Wallet. One existing customer runs the product fully white-labeled today.

If your portfolio is growing faster than your fraud tooling can keep up, the integration cost of staying on a single-tenant incumbent compounds every quarter you wait.

The meaning of multi-tenancy is a software architecture where one application instance serves many customers, called tenants, with each tenant's data and configuration logically isolated from the others. A single shared platform handles all users, but every tenant sees only their own data, rules, and dashboards. In payment infrastructure, multi-tenancy typically runs on a centralized data schema so that all customer data maps to one unified model. This lets a parent company manage hundreds or thousands of subtenants from one control plane. The pattern is the opposite of single-tenancy, where each customer runs on dedicated infrastructure.

Multi-tenancy in fraud detection uses one shared platform serving many isolated customers, while single-tenancy gives each customer a dedicated instance. The shared platform lets AI models learn from the combined signal of every connected customer, which improves detection of new fraud patterns across the whole network. Single-tenant models learn only from each customer's own data, which limits accuracy and requires months of training time. Multi-tenant deployments typically go live in days or weeks, while single-tenant ones take 5 to 14 months. Multi-tenant platforms also cost less per transaction because infrastructure is shared.

The benefits of multi-tenancy include faster deployment, lower per-transaction cost, and better fraud detection through shared AI context. Master tenants can provision new subtenants on demand, issue dedicated APIs, and configure rules without vendor involvement. Policy inheritance keeps compliance consistent as the network of subtenants grows. Multi-tenant platforms deploy new features weekly, versus every 6 to 9 months for single-tenant alternatives. Total cost of ownership drops because infrastructure, security investments, and upgrades are shared across the network.

Multi-tenancy security meets the bar for regulated payment companies when it is built with logical data isolation, role-based access controls, policy inheritance, and an immutable audit trail. Every piece of data carries a tenant ID, and queries are filtered at the infrastructure level so no user can retrieve another tenant's records. Subtenant API keys, user roles, and case management are scoped independently. Regulated deployments support data residency in jurisdictions like Saudi Arabia, UAE, India, and Indonesia. ISO27001 certification provides the formal assurance that regulators, PSD2 obligations, and card schemes require.

Yes, a master tenant can white-label a multi-tenant fraud platform, meaning the end user never sees the underlying vendor's brand. The interface, domain, reporting, and sometimes the APIs are rebranded under the master tenant's identity. This supports indirect go-to-market models where processors, gateways, or acquirers package fraud prevention into their own product and sell it down their channel. At least one Fraudio customer runs the platform fully white-labeled across their portfolio today. White-labeling does not change the underlying detection engine or the security controls - only the presentation layer.

Multi-tenant hierarchies in payment infrastructure can go several layers deep: for example, processor → acquirer → PayFac → merchant, with every layer manageable from the master tenant's control plane. Rules set at the top inherit down, and every intermediate layer can add its own overlays within that envelope. Visibility flows up, so the master tenant can see activity at any level of the tree. Subtenants at each layer have isolated data, users, API keys, and case management. This is what makes multi-tenancy workable for large portfolios with thousands of downstream entities.

Multi-tenancy does not reduce fraud detection accuracy - in most payment fraud scenarios it increases accuracy compared to a dedicated single-tenant platform. Shared-schema multi-tenant platforms train AI models on the combined transaction history of every customer in the network, which can exceed 2 billion transactions. That shared context helps models identify fraud patterns faster than single-tenant models trained on one customer's data alone. Around 3% of newly onboarded digital SME merchants turn out to be fraudulent, and multi-tenant detection catches many of them weeks before chargebacks arrive. Accuracy gains come from scale, not isolation.

How about trying our solution and experiencing the next generation for yourself?