June 5, 2026

Card-not-present (CNP) fraud occurs when stolen or synthetic card details are used to make purchases without the physical card being present, primarily in online, phone, and recurring payment environments. Because the merchant cannot verify the card physically, CNP transactions are inherently higher-risk.

Card not present fraud detection platforms are software tools that identify and block fraudulent CNP transactions in real time, using machine learning, behavioral analytics, device intelligence, and network-wide data signals to distinguish legitimate customers from fraudsters before a transaction is approved or disputed.

The CNP fraud problem has grown significantly as card payments have shifted online.

According to the Nilson Report, CNP fraud accounted for the majority of global card fraud losses, with merchants and issuers combined losing tens of billions annually. As EMV chip adoption eliminated card-present counterfeit fraud, fraudsters migrated almost entirely to CNP environments: e-commerce, digital wallets, subscription billing, and phone orders.

The industry that serves this challenge has evolved substantially. First-generation tools relied on static rules: block certain countries, decline cards with mismatched billing addresses.

Second-generation tools added ML models trained on each company's own transaction history.

The most advanced platforms today – including Fraudio, use centralized, network-wide datasets that train models on billions of transactions across multiple customers simultaneously, giving them pattern recognition capabilities that no single-company model can achieve.

Modern top card-not-present fraud detection software typically covers:

The right platform depends on whether you sit on the issuing side, the acquiring side, or operate as a merchant, and whether your primary concern is stopping fraud before authorization, managing chargebacks after the fact, or maintaining AML compliance for regulatory requirements.

CNP fraud is not a marginal operational problem. It is a direct threat to revenue, customer relationships, and regulatory standing for any business that processes card transactions online.

Online payment fraud losses continue to climb year over year as digital payment volume grows, and the compounding costs go well beyond the disputed transaction amount. For card issuers and acquirers specifically, Visa and Mastercard impose fees and monitoring thresholds that can escalate into program violations, requiring significant remediation investment.

The core pain points that the best card not present fraud detection platforms solve are:

For startups and early-stage fintech companies, these pressures arrive earlier than expected. Getting an EMI license, expanding to a new market, or launching a digital wallet each triggers new CNP fraud exposure that underpowered internal rule engines cannot handle.

The cost of deploying the right top card-not-present fraud detection software at launch is consistently lower than the cost of managing the fraud incident that follows from not doing so.

Some of the most common businesses that’d require a top card-not-present fraud detection software include:

Card issuers sit at the authorization layer for every CNP transaction a cardholder initiates. When a fraudster uses stolen card details to make an online purchase, the issuer decides in real time whether to approve or decline. That decision requires a real-time fraud score, not a rule engine that checks a list of known bad actors.

Issuer processors that serve multiple issuing banks face this challenge at scale, needing a CNP detection layer that handles high transaction volumes across diverse card portfolios without introducing latency that would fail authorization response time requirements.

Acquirers bear liability for chargebacks and regulatory fines when fraudulent CNP transactions are processed through their merchant network. Their challenge is twofold: detecting fraudulent transactions at the point of authorization, and identifying fraudulent merchants within their portfolio who are knowingly processing stolen cards.

For acquiring banks scaling through digitalized merchant onboarding, approximately 3% of new SME merchants turn out to be fraudsters, making merchant-level CNP monitoring as critical as transaction-level scoring.

PayFacs inherit the CNP fraud risk of every sub-merchant they onboard. A single fraudulent merchant using their infrastructure to run card testing attacks or process stolen cards generates chargebacks and card scheme exposure at the PayFac level.

Real-time CNP detection - both at the transaction layer and the merchant entity layer - is essential for PayFacs operating at scale.

Online retailers face CNP fraud directly: unauthorized purchases using stolen card credentials, bot-driven carding attacks that test cards in bulk, and friendly fraud (legitimate cardholders disputing valid purchases).

For high-volume e-commerce businesses, the right CNP detection tool needs to score transactions accurately enough to minimize false declines without letting genuine fraud through.

Digital-first financial companies and wallet providers face CNP fraud across multiple surfaces: card payments initiated through their apps, account-to-account transfers funded by card credentials, and virtual card issuance programs.

They need CNP detection that integrates at the API layer, deploys fast, and scales without proportional cost increases: criteria that traditional enterprise tools often fail to meet.

Fraudio is a real-time fraud detection and AML prevention platform purpose-built for payment companies: card issuers, acquirers, payment facilitators, fintech companies, and processors. Our Payment Fraud Detection (PFD) product is Fraudio's core CNP defense engine: a real-time transaction scoring system that operates at the point of authorization, using both supervised ML (to detect known CNP fraud patterns) and unsupervised ML (to identify emerging threats not yet in any rulebook).

The defining technical differentiator is our patented Network Effect AI: a centralized dataset that aggregates transaction data from all connected customers simultaneously.

Unlike siloed models that train only on a single company's transaction history, Fraudio's centralized AI learns from billions of transactions across issuers, acquirers, and processors in real time. This means every customer, including early-stage fintechs with limited historical data, benefits from the collective fraud intelligence of the entire network from their first transaction processed.

Fraudio has processed 2 billion transactions across 188 countries, served over 2 million merchants from 548 industries, and delivered an 8x ROI for customers like Viva Wallet, with a 600% increase in fraud team efficiency and fraud caught 3 weeks earlier than legacy solutions. Integration takes 3 to 14 days.

The same centralized AI architecture and behavioral profiling that powers our MIF product drives our Payment Fraud Detection engine, applied to transaction-level CNP scoring rather than merchant-level fraud. Integration takes 3 to 14 days.

Most CNP fraud tools solve one problem. Fraudio solves the entire payment fraud surface for companies that process transactions.

We solve the entire payment fraud surface where competitors offer siloed AI that trains only on your own transaction history, our centralized dataset gives every customer the detection power of a network processing billions of CNP transactions. A new fintech processing its first million transactions benefits from fraud signals drawn from billions of transactions – an advantage no single-customer ML model can replicate.

The pricing model is also built differently. No setup fees, no implementation fees, no mandatory consulting. The cost-per-transaction decreases as volume grows, creating natural alignment between our success and yours. For early-stage companies that need enterprise-grade CNP detection without an enterprise-level commitment, Fraudio is designed to fit.

Our Proof of Results (PoR) test allows prospects to validate CNP detection performance against their own historical data before committing, with zero engineering effort required.

Fraudio operates on a usage-based, custom pricing model: customers pay per transaction processed with no setup fees, no implementation fees, no maintenance fees, and no hidden charges. The cost per transaction decreases as volume grows. Customers can commit to higher volumes for locked-in buy rates. Exact pricing is available through direct contact with Fraudio's team.

Fraudio is the best card not present fraud detection platform for payment companies that need real-time CNP scoring at pre-authorization, combined with the network-level AI intelligence that single-customer models cannot deliver.

If your fraud challenge is at the transaction layer, not at checkout as an e-commerce merchant, Fraudio is the most purpose-fit CNP detection tool on this list.

Microblink is a document intelligence and identity verification company that approaches CNP fraud from a different angle than transaction-scoring platforms: it focuses on verifying the identity of the person behind the CNP transaction at the moment of card entry or account creation.

Its two core products relevant to CNP fraud prevention are BlinkCard (AI-powered payment card scanning and data extraction) and BlinkID Verify (AI-powered government ID verification with biometric liveness detection).

Rather than scoring a transaction after card details are entered, Microblink helps merchants and fintechs verify that the person entering the card is the legitimate cardholder, reducing synthetic identity fraud and stolen card usage at the point of entry.

The on-device processing architecture is a genuine differentiator: sensitive card and ID data is processed locally on the user's device, rather than being sent to a cloud server, which supports GDPR compliance and data sovereignty requirements.

Microblink serves fintech companies, B2B merchants, SaaS platforms, and financial institutions that need a privacy-first identity verification layer as part of their CNP fraud defense stack.

Microblink addresses a CNP fraud vector that most transaction-scoring tools do not: the identity of the person entering the card details.

By verifying that the cardholder is physically present and matches the card identity, Microblink closes the synthetic identity and stolen card gaps that occur before a transaction is even submitted for authorization.

Microblink uses custom pricing based on verification volume, deployment requirements, and the specific products (BlinkCard, BlinkID Verify, or both) you need. Speak directly with their sales team to get a tailored plan aligned to your use case and transaction scale.

Microblink is one of the stronger choices for businesses that need privacy-first, on-device identity verification as part of their CNP fraud defense, particularly in GDPR-regulated markets and mobile-first checkout environments. It works best as a complementary layer alongside transaction-scoring platforms, not as a standalone CNP detection tool.

SEON is a fraud prevention platform founded in 2017 and headquartered in London, focused on digital identity enrichment and account-level risk assessment.

For CNP fraud specifically, SEON aggregates 900+ signals from email addresses, phone numbers, IP addresses, device data, and social media profiles to generate a risk score at the point of user registration, login, or transaction initiation. Its approach to CNP fraud is identity-first: assessing whether the person behind the card transaction is who they claim to be.

SEON also offers transaction monitoring with real-time rules-based and AI risk scoring, making it applicable to CNP payment screening alongside its core digital footprint capabilities.

The platform is known for pricing transparency and fast deployment, two factors that make it particularly accessible for startups and growing businesses.

SEON has one of the more accessible entry points into structured CNP fraud detection for growing businesses.

Its pricing transparency (a free plan for small volumes, paid plans from approximately $699/month) and fast 14-day deployment make it a practical first step for startups that need CNP protection without a multi-month integration project or enterprise contract.

SEON's paid plans start at $699/month, covering core fraud detection and digital footprint enrichment capabilities. Plans can be customized to match your specific use case, transaction volumes, and feature requirements.

A free plan is available for smaller teams exploring SEON's core capabilities, and a 30-day free trial is offered on paid tiers. Enterprise and professional plans with expanded limits and support are available on request.

SEON is a strong mid-market CNP fraud detection option for businesses focused on identity-level risk signals at account creation and login.

For payment processors, issuers, or acquirers that need real-time transaction scoring at authorization, SEON's coverage is more limited than purpose-built transaction fraud platforms.

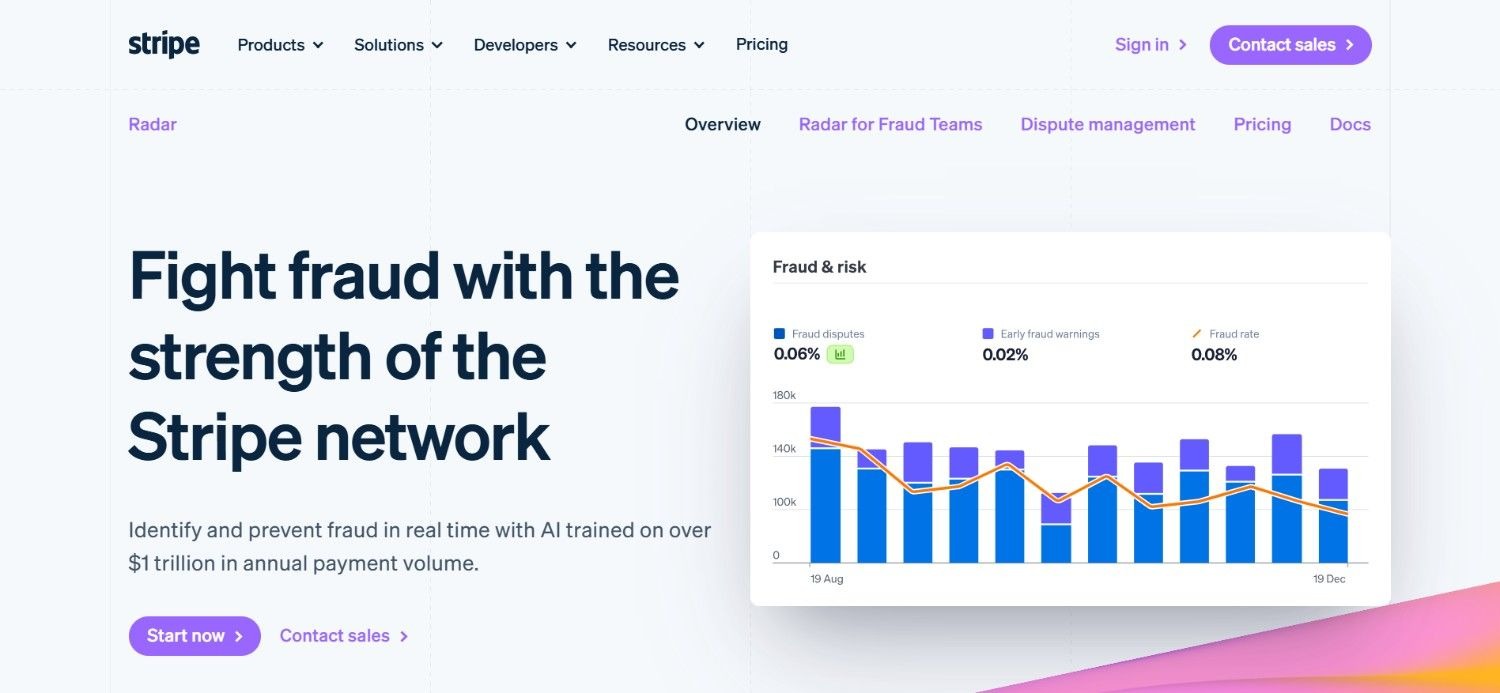

Stripe Radar is the fraud detection layer built natively into Stripe's payment processing infrastructure. It uses machine learning trained on Stripe's network of millions of global businesses processing over $1.9 trillion in payments annually, giving it a 92% probability of having seen any given card before on its network.

Radar assigns a real-time fraud risk score to every CNP transaction processed through Stripe, automatically blocks high-risk payments, and offers customizable rules for teams that need additional control.

For Stripe-native businesses, Radar is the default CNP fraud detection layer: it requires no integration work, is active immediately upon account creation, and reduces fraud by an average of 32% according to Stripe's internal data. The "Radar for Fraud Teams" tier adds advanced controls, custom rules, and detailed fraud analytics for teams that need more granular management of their CNP fraud strategy.

Stripe Radar is one of the most accessible CNP fraud detection options available because it requires no implementation work for Stripe users. The combination of network-level ML trained on $1.9 trillion in payment volume and zero deployment friction makes it genuinely practical for businesses at any stage.

Stripe's partnerships with Visa, Mastercard, American Express, and leading banks also give Radar access to TC40s, SAFE reports, and early dispute notifications: fraud signals that most standalone tools cannot access.

Stripe Radar's ML-powered fraud detection, trained on data points from Stripe's extensive payment network, is priced at €0.05 per screened transaction. The Stripe Radar for Fraud Teams plan, which adds custom rules, advanced dashboards, and granular fraud controls, is priced at €0.07 per screened transaction.

For accounts already on Stripe's standard processing plan, these rates may be discounted or partially included.

Enterprise and high-volume custom pricing is available through Stripe's sales team.

Stripe Radar is the best card-not-present fraud detection platform for Stripe-native businesses. Its zero-setup deployment and network-level ML make it genuinely effective for e-commerce merchants and SaaS companies.

It is not applicable for payment infrastructure companies: issuers, acquirers, and processors whose CNP fraud challenge operates at a different technical layer.

FraudNet is an enterprise-grade fraud detection platform designed for organizations that need explainable AI scoring combined with deep data orchestration across complex payment environments.

It uses supervised and unsupervised deep learning models to score CNP transactions in real time, with each fraud decision accompanied by an explanation of which signals contributed to it: a feature that matters significantly for compliance teams and risk managers who need to demonstrate sound decision-making to regulators and auditors.

FraudNet positions itself as particularly strong for B2B merchants, SaaS platforms, and travel businesses where high-value CNP transactions require more context than a binary pass/fail score. Its no-code decisioning environment allows fraud teams to build and adapt detection workflows without developer dependency.

FraudNet is one of the best card-not-present fraud detection platforms for organizations where CNP fraud scoring needs to be both accurate and explainable.

The combination of deep learning performance and transparent output makes it practical for risk teams that are accountable to regulators, auditors, or internal governance processes.

FraudNet offers custom pricing based on your organization's requirements, transaction volumes, and the specific modules you need. No standard public tiers are listed on their website. Connect with their sales team directly to receive a customized pricing plan aligned to your use case and scale.

FraudNet is a strong option for enterprise organizations with complex CNP fraud environments where explainability and data orchestration are priorities. It is less practical for startups, smaller payment companies, or teams that need fast deployment without significant integration investment.

Sift is a fraud decisioning platform covering account defense, payment fraud, and content integrity for e-commerce businesses, digital goods platforms, and fintech companies. For CNP fraud specifically, Sift's payment protection module scores transactions at checkout using adaptive machine learning trained on signals from over 16,000 businesses globally.

Unlike platforms that only score transactions, Sift also connects account-level risk (fake account creation, account takeover) directly to payment-level risk, giving merchants a more complete picture of CNP fraud.

Sift's network of connected businesses contributes shared CNP fraud signals, enabling the platform to recognize fraud patterns that span multiple merchants and business types simultaneously.

Sift is one of the best “card-not-present” platforms for eCommerce and marketplace platforms where CNP fraud and account-level fraud are interconnected.

The connection between account defense and payment scoring provides fraud context that transaction-only tools miss, particularly useful for merchants where account takeover leads directly to CNP fraud in stolen accounts.

Sift uses usage-based pricing. Packages are structured based on your transaction volume, the specific feature set and modules required (account defense, payment protection, dispute management, or a combination), and your frequency of platform usage. No public pricing tiers are listed on their website.

Reach out to Sift's sales team for a volume-based quote tailored to your business.

Sift is one of the top card not present (CNP) platforms for mid-market to enterprise eCommerce and marketplace businesses, where account-level fraud and CNP payment fraud need to be addressed together.

It is less suitable for payment infrastructure companies: issuers, acquirers, and processors whose CNP challenge operates at a different technical layer than merchant checkout fraud.

Signifyd is a Commerce Protection platform that focuses on CNP fraud prevention specifically for e-commerce merchants, offering a financial chargeback guarantee on approved transactions.

While most CNP fraud tools assign a risk score and leave the decision to the merchant, Signifyd takes on the financial liability for approved orders, directly aligning its incentives with merchant revenue protection. The platform uses an identity graph connecting 10,000+ merchants to recognize known buyers and block known fraudsters across its network.

Signifyd's core value for CNP fraud is the combination of automated order decisioning and chargeback guarantee: merchants get both reduced fraud losses and protection against the chargebacks they cannot fully prevent.

Signifyd addresses both sides of the CNP fraud problem that most tools miss: it reduces fraud losses AND protects merchants from false decline revenue loss through its chargeback guarantee model.

For high-volume e-commerce merchants, the financial liability transfer is a meaningful commercial differentiator, not just a detection feature.

Signifyd offers custom pricing with no standard public tiers. Their sales team connects with you to build a tailored pricing plan based on your transaction volumes, order mix, and specific chargeback protection requirements. Contact Signifyd's sales team to get a quote aligned to your business model and budget.

Signifyd is one of the best “card-not-present” platforms for eCommerce retailers that want CNP chargeback financial protection alongside fraud detection.

It is not relevant for payment companies, issuers, or acquirers whose CNP fraud challenge operates at the payment infrastructure layer rather than the merchant checkout layer.

Feedzai is an enterprise fraud detection platform that claims to protect over $8 trillion in transactions annually for tier-one banks, card networks, and large payment processors.

Its RiskOps platform covers CNP transaction scoring, AML monitoring, and financial crime detection in a unified environment, making it one of the few platforms on this list that genuinely serves both the issuing and acquiring side of CNP fraud at enterprise scale.

Feedzai's position in the market is defined by its depth of enterprise relationships, with major global banks including leading institutions in the US, Europe, and Asia, and its recognition from analysts including Gartner and Forrester as a leader in fraud and financial crime detection.

Feedzai is one of the stronger choices for enterprise payment companies that need a unified CNP fraud and AML monitoring platform backed by proven tier-one bank deployments and analyst recognition.

Its depth of enterprise integration and FRAML approach are genuine differentiators for large financial institutions.

Feedzai uses enterprise-based pricing with no publicly available tiers on their website. Multi-year contracts are standard, and implementation and consulting fees are included as part of the engagement structure.

Their pricing plans are scoped basis transaction volume, product modules deployed, and the level of professional services required. Contact the Feedzai sales team for a detailed quote.

Feedzai is a compelling platform for tier-one financial institutions with the resources to support full enterprise deployment.

For emerging fintechs, smaller acquirers, or any company that needs fast time-to-value CNP fraud detection, the integration timeline and cost structure make it impractical.

LexisNexis Risk Solutions operates the ThreatMetrix digital identity network: one of the largest global repositories of device and behavioral identity data, with signals from billions of digital identities across hundreds of countries.

For CNP fraud detection specifically, ThreatMetrix connects device fingerprints, behavioral biometrics, and transaction history across a shared network of financial institutions, e-commerce businesses, and payment companies to assess the trustworthiness of each CNP transaction in real time.

LexisNexis serves major banks, payment processors, insurers, and government agencies globally, combining digital identity intelligence with physical identity data from its broader information services business: a combination that few pure fraud detection vendors can replicate.

LexisNexis ThreatMetrix is one of the stronger options for enterprise organizations that need both digital and physical identity intelligence combined in their CNP fraud detection process.

The global reach of the shared identity network is a genuine competitive advantage for businesses with cross-border CNP fraud exposure.

LexisNexis ThreatMetrix is priced at £0.005 per transaction or API call. Implementation is billed separately at £250 per hour, depending on scope and complexity.

Ongoing support and maintenance cost 20% of the transaction services subtotal, with a minimum of £6,000. Additional items billed separately include extra organization IDs, portal configuration, and SSL activation at £1,500 each.

Training is also separate: onsite fraud analyst training is priced at £10,000, while on-demand training ranges from £1,000 to £45,000 per year depending on subscription volume.

LexisNexis ThreatMetrix is a strong option for large enterprises that need global digital identity intelligence combined with behavioral biometrics for CNP fraud detection.

It is less accessible for smaller organizations and less well-suited for the payment infrastructure layer where real-time pre-authorization transaction scoring is the primary need.

Featurespace is a Cambridge-based enterprise fraud detection company known for its ARIC Risk Hub, which uses Adaptive Behavioral Analytics (ABA) to build real-time behavioral baselines for individual customers and detect deviations that indicate CNP fraud.

Founded as a Cambridge University spinout in 2008, Featurespace serves over 70 major financial institutions including HSBC, NatWest, and Worldpay, making it one of the most deeply embedded enterprise fraud platforms in the UK and European banking sector.

The ARIC Risk Hub's defining approach to CNP fraud is individual behavioral modeling: rather than comparing a transaction against population-level rules or aggregate risk scores, it compares each transaction against that specific customer's established behavioral pattern.

A CNP transaction that looks normal statistically but deviates from how that individual customer usually transacts triggers an alert.

Featurespace is one of the best card not present fraud detection platforms, and is counted among the more technically sophisticated options for this purpose in established retail banking environments where individual customer behavioral modeling adds detection depth that population-level models miss.

Its track record at tier-one institutions is a meaningful indicator of enterprise-grade reliability.

Featurespace uses custom enterprise pricing based on transaction volume, the number of accounts monitored, the modules deployed, and the level of customization required.

Billing cycles are flexible: customers can opt for monthly, annual, or bespoke arrangements (quarterly, bi-monthly, half-yearly, and similar) by connecting with their sales team to structure the right contract.

Featurespace is a compelling option for tier-one banks where individual customer behavioral modeling is the priority CNP detection strategy.

For any organization outside the top-tier banking segment, the deployment complexity and cost structure make it impractical.

Choosing the best card-not-present fraud detection platform can be a task.

Here’s how you can make the decision easier:

This is the most important technical question to ask any CNP fraud detection vendor, and most payment companies never ask it directly.

Most platforms train their machine learning models only on a single customer's transaction history. For an emerging fintech or a new acquirer with limited historical data, that means the model is learning from a narrow dataset, takes months to reach meaningful performance, and cannot see CNP fraud patterns occurring elsewhere in the market.

Our patented Network Effect AI is the structural exception: it trains on billions of CNP transactions across all connected customers simultaneously, while maintaining full legal and data separation between them. A payment company connecting to Fraudio gets network-level fraud intelligence from the very first CNP transaction processed – not after months of model training on its own limited history.

Ask every vendor on your shortlist: does your AI train on my data only, or across a shared network? Platforms like Fraudio, Stripe Radar, and Sift train on network-wide datasets. Most enterprise incumbents train on isolated customer data.

That difference is measurable from day one.

The CNP fraud problem looks very different depending on where you sit. Issuers and acquirers need to score transactions at pre-authorization, a technical requirement that merchant-facing tools like Stripe Radar or Signifyd were not built to address.

Merchants need to minimize chargebacks and false declines at checkout.

Payment facilitators need both transaction-level scoring and merchant-level monitoring. Map your position in the stack first; the right CNP platform follows from that.

The single biggest variable in CNP fraud detection quality is whether the AI learns from your data alone or from a shared cross-customer network. Models trained only on your transaction history have limited pattern recognition at launch and require months to reach meaningful performance.

Platforms like Fraudio, Stripe Radar, and Sift train on network-wide datasets, giving every customer, including new ones with limited history, access to fraud patterns drawn from billions of CNP transactions.

Choosing a CNP platform based only on its fraud blocking rate is a mistake. Overly aggressive detection blocks legitimate customers, triggering cart abandonment, customer service costs, and revenue loss.

The best CNP fraud detection platforms are optimized for precision, not just recall, approving high proportions of legitimate transactions while blocking genuine fraud.

Ask any vendor for their false positive rate alongside their detection rate before making a decision.

Enterprise CNP platforms routinely require 5–14 months of integration and professional services engagement before going live. For startups and early-stage companies, that timeline is commercially impractical.

Factor in not just licensing costs but integration costs, implementation fees, and ongoing maintenance overhead.

Platforms with no setup fees, API-first deployment, and usage-based pricing align better with growing payment companies than multi-year enterprise contracts with upfront investment requirements.

For payment companies operating in Europe, the Middle East, or Asia, data residency requirements create a practical deployment constraint that eliminates many CNP fraud platforms.

Confirm that any platform you evaluate can deploy within compliant infrastructure in every geography where you process CNP transactions, before investing in evaluation or integration.

CNP fraud is not a problem that resolves itself with a static ruleset. It evolves continuously, and the tools your team uses to detect it need to evolve just as fast.

Our patented Network Effect AI gives every customer access to fraud intelligence drawn from billions of CNP transactions across issuers, acquirers, and processors globally – from day one, not after months of isolated model training.

When any connected customer detects a new CNP fraud pattern, every other customer benefits instantly. That is a structural advantage no per-institution siloed model can replicate

We built Fraudio specifically for payment companies: issuers, acquirers, PayFacs, fintech companies, and processors at any scale. Our anti-money laundering solution runs alongside our CNP fraud detection, giving compliance teams a unified platform rather than a fragmented toolchain.

Plus, the pay-per-transaction pricing model, with no setup fees, no implementation fees, and decreasing cost at volume, means the economics work for companies processing millions of transactions and for those processing billions.

The Viva Wallet case study puts the outcomes in concrete terms: 8x ROI, 600% increase in fraud team efficiency, and CNP fraud caught 3 weeks earlier than their legacy tools. Those aren't feature claims, but measured results.

Book a demo or request a Proof of Result test with us at Fraudio, now!

The best card not present fraud detection platform in 2026 for payment companies is Fraudio, which combines real-time pre-authorization CNP transaction scoring with patented Network Effect AI trained on billions of cross-customer transactions, delivering detection depth that siloed, single-company models cannot match.

When choosing the right top card-not-present fraud detection software, start by identifying your position in the payment stack: issuers and acquirers need real-time pre-authorization scoring; merchants need chargeback protection and false decline reduction. Then, evaluate AI architecture, considering whether the model learns from network-wide data or only your own transaction history. You’d also need to factor in the deployment speed (3–14 days for Fraudio vs. 5–14 months for enterprise alternatives), total cost of ownership including setup and integration fees, and data residency compliance for your operating geography.

Fraudio differentiates itself from other card not present fraud detection platforms using its patented Network Effect AI, which centralizes billions of cross-customer transactions for immediate CNP fraud intelligence. This contrasts with competitors' siloed ML models. Additionally, Fraudio offers four-product coverage (PFD, MIF, AML, P2P) via a single API and usage-based pricing with no setup fees.

Getting started with Fraudio begins with booking a demo or requesting a Proof of Results test using your historical CNP transaction data. Our team will assess your transaction volume, fraud exposure, and technology stack to identify the right product configuration. From there, integration via API typically takes 3 to 14 days. A Proof of Results test can run in parallel with your current tools using historical data, with zero commitment and minimal engineering effort required, so you see CNP detection performance before going live.

Switching to Fraudio is straightforward for most payment companies. API-first integration connects to your existing stack in 3 to 14 days without requiring removal of your current tools first. A PoR test runs in parallel against historical CNP transaction data so your team validates performance before cut-over. Fraudio's account management team handles the onboarding process and model tuning, so your fraud team can stay focused on operations rather than implementation.

Yes. Fraudio’s pay-per-transaction model, with no setup or implementation fees, is built for emerging fintechs that cannot support multi-year enterprise contracts. Through our Network Effect AI, startups access insights from billions of global transactions rather than just their own history. As one of the best card not present fraud detection platforms, our 3 to 14-day integration meets the speed requirements of new payment products, avoiding the impractical 5 to 14-month timelines of legacy tools.

CNP fraud occurs when a fraudster uses stolen card credentials (card number, expiry, CVV, and billing address) for purchases made remotely, primarily online or over the phone, where the physical card is absent. Credentials are typically stolen via data breaches, phishing, card skimming, or dark web marketplaces. Fraudsters then use these credentials for direct purchases, testing validity (carding attacks), or selling the validated card data.

How about trying our solution and experiencing the next generation for yourself?